F'd TX: The Restructuring

Jaw dropping absurdity. How the bankruptcy will play out.

“Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here. From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.”

- Jon Ray, bankruptcy appointed CEO of FTX

Ray made that statement under oath and punishable under perjury. Personal liability is high. Statements in bankruptcy filings usually don’t deviate from facts. That didn’t stop Ray from weighing in on the absurdity of what transpired at FTX.

Ray has 40 years of legal restructuring experience. He has overseen the proceedings of some of the largest and fraudulent bankruptcies including Enron, Residential Capital and Nortel.

I decipher the bankruptcy filings. Enumerate the jaw dropping preposterous accounts of how FTX was run. It was a melting pot of gross negligence, clown-like behavior and zero oversight. Children were let loose in a candy store filled with billions of dollars of other people’s money they could recklessly play with. I explain why the restructuring process will be very long and the recovery value for depositors uncertain. I predict how the bankruptcy will play out.

I spent the early part of my career as a restructuring investment banker and a distressed credit investor. This is the most painful thing I’ve seen.

The filings

On Thursday, November 17, 2022, FTX filed its Petitions and First Day Pleadings in the United States Bankruptcy Court for the District of Delaware. The petition usually explains how and why the company got to where it is and why it needs the court’s protection. In some cases, it also includes a plan to get out of its situation.

The FTX saga has been nothing but “normal.” The First Day Pleadings are usually filed on the first day along with the Chapter 11 filing. They were not. They were filed six days later.

FTX hurriedly filed for Chapter 11 on Friday, November 11. The Chapter 11 filing usually includes financials, board resolution, a list of top creditors, first day motions and declaration from CEO and the board. FTX’s Chapter 11 filing on November 11 had none of that. It was shocking. FTX had nothing in order.

The Petitions and First Day Pleadings, filed six days late on November 17, gave us the first glimpse into FTX’s state of affairs.

It was ugly.

The ugliness

I was awestruck reading the 32 page Petitions and First Day Pleadings. There is a litany of head-shaking, eye-rolling malfeasance:

Limited audits - FTX US and FTX.com only had audited statements for the year ended December 31, 2021. That’s uncommon for a company FTX’ size. The FTX.com audit was prepared by the “first-ever CPA firm to officially open its Metaverse headquarters in the metaverse platform Decentraland.”

Compromised financials - Ray states that he “does not have confidence” in the financial statements obtained because everything was controlled by SBF. Statements for one of the FTX venture entities has not yet been found.

$1 billion personal loan to SBF - Alameda made a $1 billion personal loan to SBF and one to FTX co-founder, Nishad Singh, for $543 million. For real?!?!

No corporate governance - There was no board. Zero oversight.

No cash controls - FTX did not maintain centralized control of its cash. There was no list of bank accounts. There was no cash liquidity forecasting. These guys literally didn’t know where the money was.

No accounting department - $16 billion in deposits and no accounting department! It was outsourced…right.

No HR - FTX couldn’t furnish a list of all its employees or the terms under which they are employed.

😉 for approval - Payment requests were approved via emojis.

Purchase of personal property - Corporate funds were used to purchase homes in the Bahamas. There is no documentation of loans made to employees. The ownership deeds of the homes were recorded in employee names.

SBF controlled access to digital assets - SBF and co-founder Gary Wang had sole access to the digital assets held by FTX International.

Software to conceal customer funds - FTX developed software to conceal customer funds.

Alameda exempt from auto-liquidations - Unlike any other FTX counterpart, Alameda did not face margin calls when its collateral value was insufficient.

$740 million recovered - Only $740 million of digital assets have been recovered. It’s unclear who it belongs to.

No decision making records - SBF made decisions using a chat messaging system that auto-deleted.

Don’t know creditors - They don’t know who they owe money to.

I am at a loss for words.

One item from this list would be reprehensible. The CEO would be immediately fired. All 15 existed at FTX! It’s jarring.

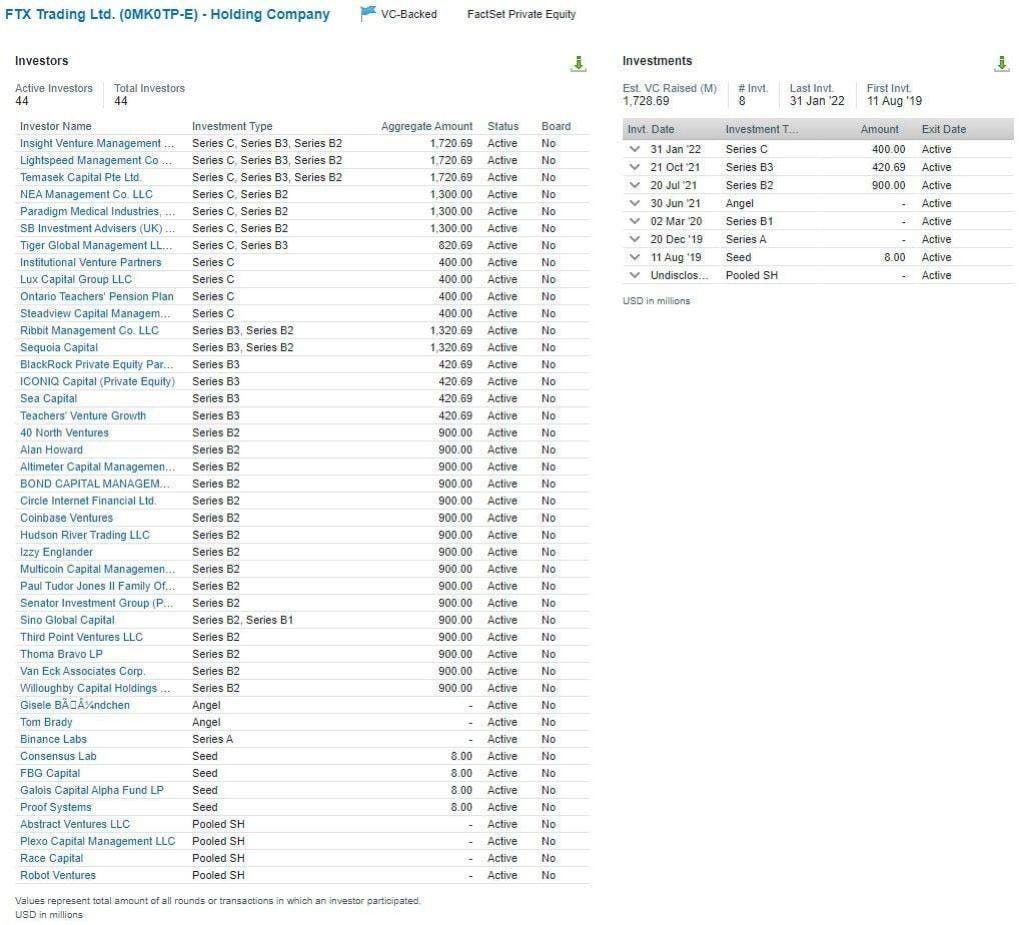

How on earth did FTX raise $2 billion from the most noteworthy investment funds in the world?!?!

Investors did zero due diligence.

I don’t blame investors for not catching the fraud. It’s really hard to do. But I do blame them for supporting SBF in his antics. Investors either never asked basic questions or turned a blind eye to the answer. That’s inexcusable. They need to be held accountable for their gross negligence.

These are all of the FTX investors. The list includes notable investors including Temasek, Tiger, Sequoia, BlackRock, Third Point and Thoma Bravo. Well known crypto funds like Paradigm, Multicoin and Coinbase Ventures were invested.

It’s going to be really complicated

Normal bankruptcy

Companies go bankrupt for two reasons: insolvency or liquidity shortfall. A company is insolvent when its liabilities are worth more than its assets. It’s forced into bankruptcy when it cannot repay its debts. A company faces liquidity squeeze when it has run out of cash to operate its business.

FTX was both. It filed for bankruptcy because it did not have funds to meet customer withdrawals. And it turns out its liabilities were larger than its assets…because it absconded $12 billion of assets (read F'd TX: The Un-Balanced Sheet).

A Chapter 11 filing implements a moratorium. Creditors cannot enforce on assets. Assets cannot be sold. Everything is paused to allow the company and creditors to devise a plan to remedy the situation. Most Chapter 11 filings do not result in the business liquidating and shutting down. Many businesses file for Chapter 11 and continue to run as a going-concern during the administration. They either re-emerge with new equity owners or they are sold. The outcome is driven by what option will yield creditors the highest recovery. Recovery is the value creditors get for their claim on the bankruptcy’s estate.

There is a clear understanding of where the assets are and who is owed what. The point of negotiation is what the assets are worth and how they should be split amongst the creditors.

FTX is not a normal bankruptcy process. Administrators do not know where the assets are, let alone their value. Nor do they know who is owed money. It’s a mess.

FTX’s bankruptcy mess

1. Assets are lost

Administrators don’t actually know where most of FTX’s assets are. That’s not normal in a bankruptcy proceeding. So far only $740 million of assets have been recovered.

2. Jurisdictional confusion

FTX and its related entities are mostly Bahamian businesses. They filed for bankruptcy in the US. The Terms of Service of FTX depositors are governed by English law. There are three legal regimes presiding over how the bankruptcy will play out.

FTX incorporated in the Bahamas because of lax regulation. FTX filed for Chapter 11 in the US because of its protections. It provides a 120 day worldwide stay on all liabilities. FTX may have used English law in its Terms of Service to exploit a loophole.

3. Unclear treatment of deposits

The treatment of deposits will be the most contested issue. Depositors are the ones that lost the most money; at least $12 billion disappeared. It is unclear what type of creditor they are and if they even have a claim on the estate. The estate is composed of all the assets of the entities that filed for bankruptcy.

That’s right. The depositors may not actually have a claim on FTX’s assets…ouch.

FTX takes deposits. But how they do that depends on if the deposits are digital assets or fiat.

The interpretation of FTX Terms of Service suggests that FTX takes legal title of the digital assets. The depositor retains beneficial title under a trust set out in English law.

This interpretation would explain why digital assets are not recorded on the balance sheets produced as part of Petitions and First Day Pleadings.

If digital assets are held in trust they are outside of the bankruptcy estate. They do not have a claim of the estate’s assets. Instead, FTX would be in breach of trust. FTX would need to return the property to its rightful owner. The “property” would be based on the number of units not their value at the time of filing. For example, if the depositor owned 1,000 shitcoins worth $3,000 at the date of filing, the depositor needs to be returned 1,000 shitcoins; even if their value has cratered.

Fiat deposits are likely treated differently. Fiat depositors are credited with FTX’s electronic money. It implies FTX takes the title of the fiat deposits. As title holder, FTX can do whatever it wants with fiat deposits as long as depositors get their money back when they ask for it.

Fiat deposits then fall within the bankruptcy estate and have a claim on FTX’s assets.

To make matters more confusing, what happens with digital asset deposits that were later converted into fiat? Or vice versa? Digital assets appear to have been held by FTX pooled accounts. So depositors really have claim to their proportionate share of the contributed assets to the pooled account. It will be challenging to determine who owned what in the pooled asset. FTX updated its Terms of Service May 12, 2022. Prior to that, the Terms of Service were governed by the laws of Antigua and Barbuda. The details were scant. Customers automatically agreed to the revised Terms of Service by using FTX services.

I suspect digital asset depositors will be the largest claimant. They will devise a strategy to get their money bank.

They could claim the assets are held in trust, as the Terms of Service suggest, and that FTX was in breach of trust. The benefit of this approach is that they need to be paid back in full ahead of others. The drawback is twofold. First, the deposits have disappeared. They’re banking on being able to claw them back. Second, depositors could get back the full amount of token units they owned, but depending on what was owned, they could now be worthless.

Alternatively, digital asset depositors may argue their assets were not held in trust. FTX in fact took title of the digital assets. The benefit of this strategy is that digital asset depositors would have a claim on the bankruptcy estate. The drawback is their claim would likely be pari-passu with other creditors.

There is a scenario where digital asset deposits are treated as held in trust. Lost deposits are barely recovered. Lenders and equity holders of FTX get more money back than digital depositors do because they have a claim on the bankrupt estate. Conniving creditors could push for this interpretation at their benefit and the detriment of digital asset depositors. Imagine the backlash if this was to play out.

The administrator may decide that depositors have equal claim because that they can’t untangle the web of coagulated assets.

4. Structurally separate entities all intertwined

There are four separate standalone entities that comprise the SBF complex. FTX US (known as West Realm Shires), Alameda, the venture business (known as Clifton Bay Investments) and FTX.com (known as FTX Trading Ltd.). They all have ring fenced assets and liabilities. Creditors of one entity only have claims to the assets of their entity. Companies are purposely structured this way so that if one entity is sued or files for bankruptcy, the remaining businesses are unaffected.

FTX has intercompany loans between the various entities. Furthermore, assets were probably illegally moved between entities. The separate entities became intertwined. It may all be treated as one for the bankruptcy proceeding.

The Petitions and First Day Pleadings include balance sheets for all four entities as of September 30, 2022. Although the administrator states they cannot be relied upon, I think their liabilities are somewhat correct. It is unlikely the liabilities are overstated.

I have recreated the balance sheets here for easier viewing. Intercompany loans are not shown on the disclosed balance sheets. Secrets will be revealed analyzing intercompany loans.

Tracing loans between the entities will uncover who is owed what. For example, Alameda has $5 billion of third party debt. Alameda lent $4 billion; $1 billion to SBF, $0.5 billion to co-founder Nishad Singh, and $2 billion to the entities that comprise of FTX’s venture portfolio.

If there are no intercompany loans between FTX, FTX US and Alameda, then it stands to reason that the $5 billion third party creditor has sole claim over the $1.5 billion of personal loans and $2 billion that funded the FTX ventures portfolio. That would be a really bad outcome for depositors.

If there are intercompany loans into Alameda, then it's a different story. Cash is fungible. The third party creditor to Alameda and the entity lending to Alameda via intercompany loans have equal claim on the assets that were funded by the loans Alameda issued.

5. Clawbacks will be thorny

A court can order money to be clawed back to the estate due to preferential and fraudulent transfers. Clawbacks increase the size of the estate and improve the recovery value. SBF was well known for his generous donations to politicians and pet projects. The SBF complex contributions are being tallied. It will be in the hundreds of millions ($40 million to 2022 midterms, $70 million to DC lobbying, $190 million to his foundation, $128 million to a PAC).

Those contributions could all be clawed back if it’s proven they were funded by customer deposits. Politicians and non-profits were the recipients. They won’t easily give it back. In many cases, it’s probably already spent. The recipients are non-for-profit entities. They don’t have the means to pay it back. It’s unclear what will happen. I can’t imagine a non-profit or politician doing a successful fundraiser to pay back FTX.

Alameda planned to borrow up to $750 million from DeFi protocols. It’s conceivable that Alameda’s DeFi creditors received an illegal preferential treatment at the detriment of depositors. DeFi loans are liquidated as soon as a predetermined collateral threshold is crossed. The collateral is sold. The loan is repaid in full. The issue is that the collateral may have been funded by FTX depositors. In which case, the DeFi loan would have a claim on the estate like everyone else. Except in this case, since DeFi loan is governed by an automatic smart contract, it was automatically liquidated. It got paid back in full when it should share in the loss like all other creditors. Preferential payments can be clawed back. The issue is, the DeFi smart contract cannot be reversed. Unlike traditional lenders, the DeFi protocol has no entity to take to court to claw the preferential payment back. It’s a shortcoming of DeFi that depositors will bear the unfair consequences of.

6. Bahamian process interfering

There are two competing processes going on at the same time. FTX filed for bankruptcy in the US and in the Bahamas. One jurisdiction normally cedes to the other. The US is usually the jurisdiction of choice. Of course, in FTX’s case that has not happened.

Jon Ray is moving ahead with the Chapter 11 filing in the US. He has made it clear SBF is in no way associated with the business anymore. However, SBF appears to be cozying up to the Bahamian administrators in hopes of influencing the process. SBF has stated his biggest regret is filing for Chapter 11. He wants to raise money, make depositors whole and run the business again.

US filings indicate that the hack the evening of Friday, November 11, several hours after FTX filed for Chapter 11, was authorized by Bahamian authorities. This was in violation of Chapter 11 proceedings.

The good news is part of the “hack” may not have actually been a hack after all. The bad news is the US and Bahamian administrators are in a pissing contest.

7. Side door shenanigans

Customers withdrew $5 billion of deposits in the days before FTX halted withdrawals and subsequently filed for bankruptcy. Treatment of these deposits will be a contested issue. Creditors will claim those who withdrew received a preferential treatment. A judge will determine if that’s the case. In theory, the $5 billion could be clawed back if it was a preferential treatment. In practice, it will be challenging to force perhaps tens or hundreds of thousands of depositors from all over the world to send their withdrawals to the FTX estate in exchange for less than 100% of their deposited value.

Several side deals took place right before FTX filed for Chapter 11. All should be unwound if they resulted in some parties getting preferential treatment. FTX depositors who owned Tron tokens could swap them for new Tron tokens not stuck in FTX. Bahamian depositors were still able to withdraw their funds once FTX had halted withdrawals. The Serum network was forked. Serum token was one of FTX’s largest assets valued at $2 billion. Again theory and practice may be two different things. If any of these actions resulted in creditors being made worse off, they would be reversed. But, they will be nearly impossible to reverse.

8. No precedent

There are no precedents set by prior crypto bankruptcies to guide how things should work.

9. FTX bailouts will restructure

FTX’s deal to acquire Voyager out of bankruptcy has been canceled. BlockFi is now likely filing for bankruptcy after its bailout from FTX is off the table. Voyager and BlockFi are likely lenders and borrowers to different entities in the SBF complex. They’ll be one more thorn to parse through.

How it plays out?

The administrator first needs to get FTX’s house in order. Discover where the assets are. Determine how much is owed. Categorize the different creditors based on their seniority and asset claims. Then attempt to value the assets. Devise a plan to get the asset back, harvest their value and distribute them accordingly. Get everyone to agree to said plan. Execute.

I make it sound so simple. It’s anything but.

There are four tools to create value for creditors:

Liquidation - Sell whatever assets are available today. It’s the fastest process but will yield the lowest recovery value.

Clawbacks - Get back funds that were fraudulently disbursed. It’s an expensive time consuming process. There are $12 billion of deposits missing. Clawbacks will be the biggest driver of recovery values.

Harvest assets - The venture portfolio has at least $2 billion of assets. In time, the portfolio could be worth a lot more. If depositors have claim to the venture portfolio, it could help recovery values.

Going concern - Operate FTX’s once profitable exchange. Creditors become the new equity holders of the restructured FTX. The proceeds from operating the exchange compensate them for their losses.

I believe the most likely scenario is a combination of all four. The liquid assets will be sold to help fund the bankruptcy proceedings. The majority of the effort will be clawing back assets. The venture portfolio will sit idle for years in hopes of future value. FTX may start operations again under a different restructured entity. The creditors will be its new owners.

Today’s creditors are unlikely to be FTX’s future creditors if the bankruptcy is a lengthy process. I suspect it will be. Existing creditors will sell their claim to hard nosed distressed funds who will parse through the assets and legalese to find value.

Creditors may be offered a selection of different assets. They may choose to get part of their remuneration from any combination of the clawback pool, the venture portfolio and equity in restructured FTX.

It’s impossible at this stage to assess recovery value without proper financials and a better view of how depositors will be treated. In time, we’ll better understand both and how the proceedings will unfold.

There will be opportunities parsing through the wreckage. Unfortunately, the pain of depositors will not be remedied anytime soon, if ever.

Stay curious.

Research for this piece was informed by @wassielawyer, @gonbegood , @ThomasBraziel

Follow me on Twitter @samuelmandrew for my latest.

It appears that the pissing contest with the Bahamian regulator is at least somewhat resolved now with the Delaware court taking the FDM Chapter 15 case that was filed in SDNY.

Great summary, ty