F'd TX: The Un-Balanced Sheet

$12 billion of customer deposits vanished; here's how it happened

FTX imploded, filed for bankruptcy and likely misused client funds…and for the cherry on top, Friday night it got hacked draining what little liquid assets were left.

The FTX debacle was plastered all over mainstream media. Crypto finally became mainstream!…but for all the wrong reasons.

Less eye-catching was the Financial Times leaking FTX’s balance sheet. It’s a complete and utter mess. I dug through the wreckage.

I’ve spent over a decade analyzing balance sheets. I’ve never seen anything like this. It’s so bad, it’s farcical. It’s riddled with voodoo accounting. Strewn across the middle is a note seemingly from SBF “wish[ing] I could do things differently than I did.”

The most troublesome thing: it indicates that $12.2 billion of customer deposits vanished before last week’s implosion. That spells fraud of seismic proportions.

How bad is it?

Like, so bad.

A few nuggets to salivate your taste buds:

The illiquid asset value of $8.9 billion is mostly bogus. It is made up of fabricated assets and assets that don’t belong to FTX.

FTX had only $900 million of assets to cover $9 billion of liabilities days before it filed for bankruptcy.

There is a negative $8 billion line item excluded from the asset and liabilities calculations called “Hidden, poorly internally labeled "fiat@" account.” WTF is that?

This is FTX’s balance sheet. I recreated it here.

Wait, is this balance sheet legit?

I think it is. The FT is a reputable source. Meta data suggests SBF is the owner of the file. FT sources confirm this document was shared with prospective investors last week when FTX was clamoring for funds.

No wonder they all passed.

How is it supposed to work?

Balance sheets tabulate everything a company owns and owes. The assets represent what is owns. The liabilities and equity represent how it funded the purchase of its assets. Assets = Liabilities + Equity. They must balance, hence the name.

The simplistic exchange model is as follows. I deposit $100 worth of ETH onto FTX. The $100 of ETH is a liability for FTX. They need to give it back to me when I ask for it. I trade my ETH for BTC through FTX. FTX earns revenue by charging me a trading fee. FTX’s liability changes to $100 worth of BTC once my trade is executed.

It gets a bit more complex. In the simplified example, my $100 of BTC also becomes an asset for FTX. They use it to generate revenue. No different than a bank uses the money I deposit with them to fund a mortgage for someone else. Instead of funding mortgages, FTX uses deposits to provide margin to other clients and invest.

The key in this model is to have enough liquidity on hand to meet customer withdrawals. Regulation dictates how much liquidity reserves banks need to have on hand to meet customer withdrawals. In times of crisis, banks can borrow money from the Federal Reserve to ensure they always have enough liquidity to meet customer withdrawals. This regulated system prevents a run on a bank and guarantee customer deposits. This mechanism does not exist in the unregulated crypto industry.

FTX’s liabilities should show deposits from customers and the debt that FTX has borrowed from third parties. The asset side of its balance sheet should show what FTX has done with customer deposits and any debt and equity raised.

In our simplistic example, FTX balance sheet would show $100 worth of BTC as a liability (i.e. my deposit) and $100 worth of BTC as an asset. They’re matched 1:1. In our more complex extension, there would still be $100 worth of BTC as a liability. The assets would be slightly different. There may be $30 worth of BTC and $70 worth of other assets. The $30 worth of BTC are the reserves FTX is holding to fund potential withdrawals. The $70 of other assets is FTX deploying capital to generate revenues.

So what does FTX’s balance sheet actually look life? Let’s analyze FTX’s liabilities and assets.

FTX’s liabilities

FTX has $8.8 billion of liabilities 60% of which are in USD. The split is as follows:

I suspect the bulk of the EUR, USDT, ETH, BTC and USD highlighted above worth $8 billion represent client deposits. It is possible some of these liabilities are loans FTX borrowed.

It’s been widely sourced, including from WSJ, that FTX had $16 billion of deposits.

Then why does FTX not have $16 billion of liabilities?

A few possible explanations:

1. Hidden, poorly internally labeled "fiat@" account

Recall the mind boggling negative $8 billion entry “Hidden, poorly internally labeled "fiat@" account.” It could be $8 billion of customer deposits that FTX had not accounted for. How you miss $8 billion, 50% of your funds, and no one notices is beyond me. It would support the accusations that FTX had a backdoor accounting system that transferred $10 billion to Alameda.

If the hidden $8 billion are unaccounted client deposits (i.e. liabilities), then combined with the $9 billion of reported liabilities, the $16 billion total deposits figure makes sense.

2. Balance sheet timing

The balance sheet is dated Thursday, November 10. The spreadsheet notes that FTX faced $5 billion of withdrawals over the prior weekend. The $9 billion liability figure may be net of the $5 billion withdrawals. If that’s the case, then there was $14 billion of total deposits.

The bigger point

THERE IS AN ENTRY FOR A HIDDEN $8 BILLION!!!!

It’s not clear from the spreadsheet if the negative $8 billion should be included in liabilities or deducted from equity. It’s not at all a normal entry. Matt Levine said it best:

“The result of adding or subtracting those numbers [the -$8 billion] with ordinary numbers is not a number; it is prison.”

It’s jarring that such a figure would be on a balance sheet. FTX loses all credibility. The fraud alarms ring at deafening tones.

FTX’s assets

FTX reported $19.6 billion assets “before last week,” which means before November 6. FTX disclosed $10 billion of assets on November 10. The $9.6 billion drop in asset value in 5 days was due to a $5 billion drop in the value of FTT tokens, $3.2 billion drop in SRM and $1.2 billion drop in SOL.

The $19.6 billion figure should be further reduced by the $0.5 billion Robinhood position. FTX does not own it. Emergent Fidelity owns it. Emergent Fidelity is owned by SBF. It is not one of the 134 entities listed on FTX’s bankruptcy filing.

The table below illustrates a summary of FTX’s reported balance sheet. It shows FTX’s state before things imploded on roughly November 5. FTX’s position while things were imploding, but before it filed for bankruptcy, on November 10. The Adjusted November 10 figures incorporate the drop in asset values and removes the Robinhood investment. The delta column shows what changed in value between the Reported November 5 and Adjusted columns. The Adjusted November 10 column is the best representation of FTX position right before it filed for bankruptcy.

Let’s take a closer look at FTX biggest assets individually.

SRM token

SRM is a $5.4 billion asset on November 5 and a $2.2 billion asset on November 10.

SRM is the token for the Serum Network. Serum is building a decentralized exchange on the Solana network. SRM token holders get discounted trading fees and a portion of the trade revenues of Serum’s exchange. FTX heavily promoted SRM.

If this sounds similar to how I described the FTT token in F'd TX: The Saga; it’s because it is. The “magic” that Alameda and FTX created with the FTT token was recreated with SRM…uhh ohh.

There are gigantic issues with this asset. Most notably it proves FTX client deposits are not at FTX anymore.

1. It’s completely illiquid

SRM’s average daily trading volume, prior to the FTX debacle, is $4 million. FTX couldn’t possibly sell $5 billion worth of SRM into such a minuscule market. Low volumes allow FTX to control the SRM price.

2. It’s value is fabricated

Serum, or really, FTX created SRM. For simplicity sake, say Serum issued 10 billion tokens. At launch, Serum sold 1 million tokens for $2. Serum’s market cap is $2 million ($2 x 1 million tokens). SRM's fully diluted market cap, in crypto terms, is $20 billion ($2 x 10 billion tokens). FTX’s remaining tokens, all 9,999,000,000 of them are worth $19,998,000,000. Poof! FTX has a $20 billion asset on its balance sheet.

Wait what?!?!?

I made up these extreme numbers to prove a point. This mechanism and shoddy accounting allows FTX to create a large asset on its balance sheet.

There is value in SRM. Serum is a real network. Token holders have governance rights and are owed a portion of trading revenue. It’s kind of like owning a stock. But the point remains, FTX was able to fabricate the value of SRM out of thin air. It then plopped that asset value on its balance sheet.

3. No money was used to buy SRM

The elephant in the room is that no money was used to buy SRM. FTX minted SRM for itself. Recall the balance sheet is supposed to show the assets that the liabilities funded. FTX got deposits from clients (i.e. liabilities) and used those assets for…for….I don’t know.

It was definitely not used to purchase $5 billion of SRM.

FTX has the liability portion, the $5 billion worth of client deposits, on its balance sheet. But it does not have a corresponding asset on its balance to explain what it did with the $5 billion of deposits.

We’re certain no money, either customer funds or FTX own money, was used to buy SRM. Then what happened to $5 billion of customer deposits?

FTX’s accounting of SRM proves that $5 billion worth of customer funds went missing.

FTT token

I explained how the FTT token works in F'd TX: The Saga. The gist of it; it’s exactly like SRM. FTX created it. Issued it to itself and Alameda. Pumped up the price. Controlled the supply. Voila, like magic a $6 billion asset on the balance sheet.

Lightning did strike twice. FTX fabricated the balance sheet value of both SRM and FTT.

The conclusion is the same as SRM. FTX did not use money, either its own or customer deposits, to buy FTT. FTX received FTT for free.

So if FTX did not use deposits to buy FTT, where did the deposits go?

They disappeared.

SRM + FTT = missing client deposits

If you’re keeping score, FTX’s two largest assets worth a combined $11 billion two weeks ago consisted of fabricated asset values. No money, denominated in crypto or otherwise, either belonging to clients or FTX, was used to purchase them. They were used to hide $11 billion worth of customer deposits that vanished from FTX.

FTX does not have tangible assets, crypto or otherwise, to match its client deposits. The accounting of SRM and FTT proves that customer deposits went missing. If that was not the case, there would be $11 billion worth assets FTX used money, either its own or client deposits, to acquire on the balance sheet.

Recall how the balance sheet should look. Applying the simplistic example I gave earlier where assets and liabilities are matched 1:1, there should be $11 billion of assets held for customers instead of the SRM and FTT assets. The asset held for customers would be the various tokens FTX clients bought with the deposits they made. That’s how Coinbase reports its client deposits. In the more complex extension where assets and liabilities are not quite matched 1:1, there could be $4 billion of assets held for customers and $7 billion of assets deployed for revenue generating purposes for example. But none of that exists. Only $11 billion of a phantom asset.

SOL

Solana is a blockchain. It offers faster and cheaper transactions than Ethereum. Its token is SOL. It’s a legitimate project. Its token has value. However, Solana was part of the FTX hype machine. SOL dropped 57% to $15 due to the FTX debacle. The market feared FTX would dump its SOL, one of its largest semi-liquid investments. FTX was no longer in a position to promote and invest in the Solana ecosystem. Some derivative DeFi tokens used on Solana could only be traded through FTX. Those tokens became worthless.

The SOL asset is impaired, but has value. Money was used to purchase it.

So how big is the hole?

FTX had $19.6 billion of assets on November 5 before panic ensued. We don’t know the exact split of its liabilities and equity on November 5. But we do know that combined they must equal $19.6 billion. A balance sheet must still balance. It is reasonable to assume FTX had liabilities of $16 or so billion, which reconciles with the $16 billion widely quoted deposit figure. The remaining few billion is FTX’s equity value.

We know that FTT and SRM are phantom assets. MAPS, which I have not touched on in detail, is also a phantom asset. The vast majority, and likely all, of FTT, SRM and MPS was issued for free to FTX. No money, including crypto equivalents, funded by customer deposits or FTX own money, was used to acquire them. So where did the money go?

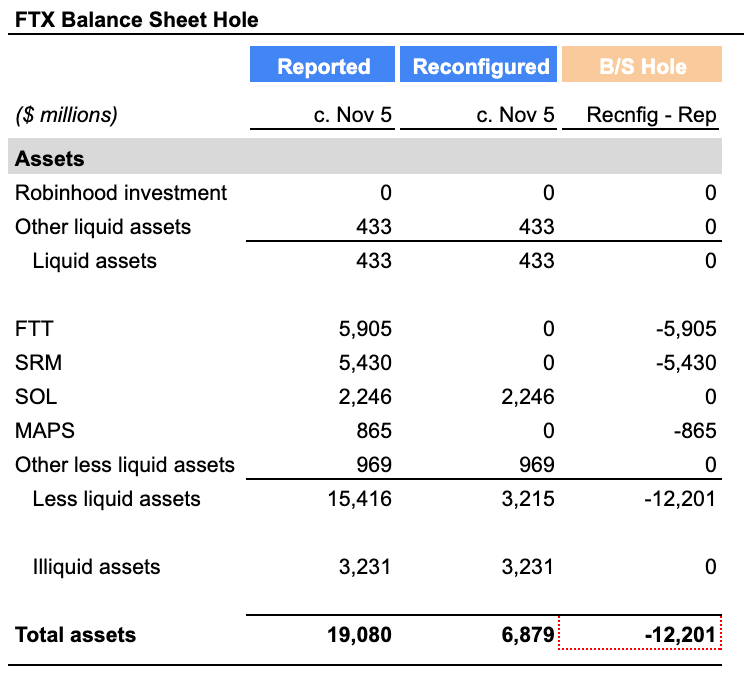

There is a liability (i.e. customer deposits) associated with those three tokens but no corresponding tangible asset. The total asset value of those three assets is a whopping $12.2 billion.

The table below shows FTX reported balance sheet on November 5, excluding the Robinhood investment it does not own. The Reconfigured column shows the balance sheet on November 5 excluding the phantom assets. The B/S Hole column is the difference between the Reported and Reconfigured columns. It shows the gapping $12.2 hole.

There are $12.2 billion worth of customer deposits that are unaccounted for. FTX hid the gargantuan hole by three phantom assets.

What does this all mean?

FTX absconded $12.2 billion worth of customer deposits. Poof. Disappeared into the abyss.

Investigators will eventually find where it went. I suspect Alameda got some of it. But I don’t think all of it. Alameda had $9 billion of tangible assets (excluding its FTT holding) and $7 billion of loans. I don’t think Alameda could have swallowed $12 billion. Alameda’s balance sheet would be bigger if it had taken all of it.

Perhaps part of the $12 billion funded SBF’s spending.

Wherever it went, don’t count on getting it back.

It appears that FTX processed $5 billion of withdrawals before this balance sheet was compiled. FTX likely sold other assets not shown on this balance sheet to fund the withdrawals. The $5 billion of withdrawals plus the $12 billion absconded accounts for the $16 billion of total deposits. It implies there are no deposits left at FTX. It explains why they hastily filed for bankruptcy.

The outlook is bleak for creditors. They will fight over the scraps of assets in a long bankruptcy process.

The saga continues. The pain and damage are not over. The hunt for the missing funds is on. FTX and SBF should be prosecuted. This is fraud.

We’re left wondering how a company founded by a wonder-kid and backed by the world’s most prominent funds became so big built on smoke on mirrors.

Stay curious.

Follow me on Twitter @samuelmandrew for my latest thoughts.

Insights for this piece were derived from @matt_levine’s great work.

Nice work! I’m going to include this in my weekly rundown. Thanks so much for publishing it 😀