W(E)TF

Implications of a spot BTC ETF

Investment giants want to invest in BTC. BlackRock, an industry titan, wants to launch a spot BTC ETF. BlackRock is the largest asset manager with $9 trillion of assets under management. Several asset managers followed suit. When BlackRock acts, the market pays attention.

So why is this time different?

What are the implications for BTC and crypto?

What’s the read across for Grayscale?

Let’s dig in.

What happened?

On June 15, 2023, BlackRock filed an S-1 to list a spot BTC ETF. Invesco and Wisdom Tree, investment managers, who manage $1.5 trillion and $65 billion of assets respectively, filed for similar ETFs in the following days.

These are plain vanilla ETFs. Investors deposit money in the ETF, the ETF buys and custodies BTC on behalf of investors. The ETF sells BTC whenever the investor wants their money back. $6.5 trillion is invested across thousands of US ETFs. ETFs have grown in popularity. The amount invested in them has grown 65x over the last 20 years. They are a low cost and easy way to own commodities and baskets of stocks and bonds. ETFs are one of the best financial innovations of the last few decades. They make investing easier for retail investors.

Why is this time different?

A BTC spot ETF was first attempted in the US in 2012 by Gemini. Several managers have tried and failed since. The SEC has denied all 33 spot BTC applications. Grayscale, the manager of the Grayscale Bitcoin Trust (“GBTC”), is suing the SEC in order to convert its ETF-like structure into an actual ETF.

Quick background on GBTC for context

GBTC is the closest thing to a US spot BTC ETF. It’s a listed vehicle. Investors can own BTC through GBTC. Grayscale buys and custodies the BTC on behalf of investors. GBTC owns $19 billion of BTC on behalf of GBTC holders. GBTC has a market cap of $13 billion. That’s a problem. GBTC’s market cap is only 67% of the actual value of the BTC it owns.

GBTC’s market cap does not equal the value of the BTC it owns because GBTC shareholders cannot redeem. Unlike a typical ETF, GBTC cannot simply sell the assets it has to fund withdrawals. GBTC is not an ETF. It’s a structure that mimics an ETF but does not have the critical feature of easily enabling redemptions.

Back to why this time it’s different

There are two reason why this time it’s different:

1. It’s BlackRock

BlackRock is in a league of its own. It’s an industry giant with $9 trillion of assets under management. BlackRock is the largest ETF manager. It has a third of the market. BlackRock’s record of successfully launching ETFs is 575-1. Larry Fink, BlackRock’s Founder and CEO, has as much clout as Jamie Dimon. Fink and Dimon are on a whole other level of influence. Fink is also a well connected Democrat.

BlackRock doesn’t decide to do this on whim. They don’t pick losing battles. They’re more in the know and connected in the ETF industry than anyone else.

If it was anyone else filing, maybe with the exception of Vanguard and Fidelity, it would be a different story.

2. BlackRock claims to address the SEC’s spot BTC ETF concerns

The SEC has stated that in order to approve a spot BTC ETF three things need to be present:

A regulated market of

“significant” size for which there is a

“surveillance sharing agreement”

The SEC has approved a futures BTC ETF. The approval was on the basis that the Chicago Mercantile Exchange (“CME”), which is a regulated market where futures are traded, is of “significant size” for which there is “surveillance.”

The argument seems contradictory and wound up in technicalities.

How can the CME be a “regulated market of significant size” for BTC futures, but not for spot BTC? Futures derive their price from spot.

And if the spot market is not regulated and surveilled, how could the CME detect and deter any potential fraud or manipulation in the spot market?

Those questions are the crux of the Grayscale suit against the SEC. Craig Salm, Chief Legal Officer at Grayscale, laid out the SEC’s reason for not approving Grayscale spot BTC ETF and the challenges BlackRock will have in getting approval in this tweet thread:

The key difference in BlackRock’s ETF filing versus prior ones is BlackRock’s introduction of a surveillance mechanism.

The unnamed “US BTC Spot Market Platform” is likely Coinbase. BlackRock’s argument is that (i) the Coinbase exchange is a marketplace (ii) of “significant size” and (iii) Nasdaq will surveil transactions as part of a “surveillance sharing agreement.” The surveillance agreement BlackRock proposes is similar to arrangements the SEC has approved with other commodity ETFs.

But…

Coinbase is not a “regulated” market. The SEC is currently suing Coinbase for not being a regulated market. It’s also debatable if Coinbase’s exchange is of “significant” size. Binance dominates spot trading volumes globally. Binance does 10x more volumes than Coinbase (see below).

BlackRock’s surveillance agreement mechanism is likely enough to address the SEC’s desire to have a “surveillance sharing agreement.” But BlackRock’s proposal doesn’t address the fact that Coinbase’s exchange is not regulated. And Coinbase’s exchange is likely not of “significant” size.

So why is this proposal that different?

Back to point number 1. It’s BlackRock. BlackRock is definitely aware of these potential shortcomings. BlackRock knows ETFs better than nearly anyone.

If the market is defined as US BTC volumes, then Coinbase is a “significant” market. But I don’t know what the angle is on the regulatory front.

How will this play out?

The SEC has at most 240 days to reach a decision. The approval or denial of BlackRock’s spot BTC ETF should be known by mid-February and possibly earlier.

I believe it’s more likely than not that a spot ETF gets approved. My rationale is as follows:

1. SEC war on all fronts

The SEC is fighting an all out war against crypto. Its methods are being challenged in the court of public appeal, Congress and the judicial system. The SEC is losing political goodwill on Capitol Hill.

The SEC has stated BTC is not a security. It’s a commodity. ETFs exist for all sorts of commodities. Heck, a futures BTC ETF even exists. The reasons for not approving a spot BTC ETF are technical in nature. Experts in the field and regulators can surely compromise on something that enables investors to buy what they want while giving them adequate disclosures and protections.

The reality is, preventing GBTC from being an ETF caused way more carnage than had it been an ETF all along (read DCG's Downfall).

I think the real reason to not have a spot BTC ETF is to keep crypto at bay.

The SEC may no longer want to fight the spot BTC ETF fight. Their resources are constrained. They’re more focused on arguing non-BTC tokens are securities and suing exchanges for operating as unregulated exchanges, broker dealers and clearing agencies.

The SEC has a way out of this fight. The SEC can save face by stating that “BlackRock’s ‘surveillance agreement’ solved what other ETF filings did not.” The SEC gives crypto a win. The pressure on the SEC dissipates. The SEC comes out a winner claiming “look, our regulatory methods put crypto in the hands of adults…BlackRock…the public can now safely invest in spot BTC ETFs. We did our job. You’re welcome.”

2. Bad look for BlackRock if ETF doesn’t get approved

There is some reputational harm in BlackRock filing for a spot BTC ETF and not getting it approved. Eric Balchunas, one of the foremost ETF experts, explained that BlackRock filing creates a wave of other managers filing for similar ETFs, especially since it’s BlackRock filing. ETF filings are largely the same. Once one is approved, another following the exact same framework will also get approved. The one that’s in the cue first, gets approved first. The others need to wait in line. There is an advantage to filing first. The first one to market is the only one in the market for a period. It gets a disproportionate amount of investor capital.

The wave of additional filings causes more work for the SEC. BlackRock is aware of this dynamic. I don’t think BlackRock would file knowing its chances of approval are low. The result would be unnecessary frustrating additional work for the SEC. BlackRock would lose goodwill with the agency that regulates it.

I think there was some back channeling that went on to gauge the likelihood of approval.

3. Grayscale may win its case against the SEC

The industry has been following Grayscale's suit against the SEC. The ruling is expected this fall. One of two things may have happened:

BlackRock thinks the SEC will lose the case. It’s preempting the loss by submitting an ETF application.

The SEC thinks it will lose the case. The SEC backchanneled to the industry to get ready.

4. BlackRock doesn’t play around

BlackRock has launched 576 ETFs, all but one was approved. Perhaps none are as consequential as the spot BTC ETF. BlackRock thrusted itself into the crypto arena at a time when the political discourse is most challenged. It didn’t need to do this. It didn’t make this decision lightly. The reputation risk is too high for BlackRock to file just another ETF on the off chance it gets approved.

So what?

The implications of a potential spot BTC ETF are far reaching.

1. A US spot BTC ETF could be coming

It likely is different this time. The odds are only slightly in favor of an approval. But that’s higher than they have ever been.

2. BlackRock’s ETF submission (and potential approval) helps legitimize crypto

This is not a flash in the pan. BlackRock is not attempting an ETF for an asset it thinks won’t exist in a few years time. The reputational risk with regulators and clients is too great. I suspect BlackRock is not just thinking about BTC, but ETH as well.

Larry Fink writes an annual letter outlining his thoughts on the investing landscape, markets and emerging trends. His letters are seminal literature for financial markets participants. BlackRock essentially created ESG investing. Fink’s 2023 letter highlighted the benefits of blockchain technology and his concerns over the US lagging in its innovation.

3. US tradfi is pushing for crypto regulation

Some version of regulated crypto is happening in the UK, Europe, Hong Kong, Japan and Singapore. UK Prime Minister Rishi Sunak is outspoken on his desire to make London a crypto hub. The European Parliament has passed the MiCA legislation making the EU the first major jurisdiction in the world to pass comprehensive crypto law. Hong Kong has introduced its own legislation to regulate crypto. Japan has passed crypto legislation. Japanese regulation prevented FTX Japan clients from losing money. Singapore has been passing crypto regulation since 2020.

The question is not whether or not a spot BTC ETF is going to happen, the question is where. Spot BTC ETFs already exist in Canada.

American financial institutions don’t want to cede to their global competitors. BlackRock filing for a spot BTC ETF may be a signal for American regulators to get their act together.

4. A successful BlackRock ETF approval means GBTC can convert to an ETF

A BlackRock spot BTC ETF approval means Grayscale, and any other licensed manager, should be approved for a spot BTC ETF operating under the same framework. It means GBTC could convert to an ETF and compress the discount. That’s huge.

The SEC can’t play favorites. It cannot approve BlackRock’s spot BTC ETF submission and deny someone else’s identical filing.

The BlackRock filing is a concerted effort. Technically it's the Nasdaq that petitioned the SEC in a 19b-4 filing introducing the “surveillance mechanism.” If the mechanism is approved, it would apply to all ETFs filing for a spot BTC ETF listing on the Nasdaq. It’s not a BlackRock specific thing.

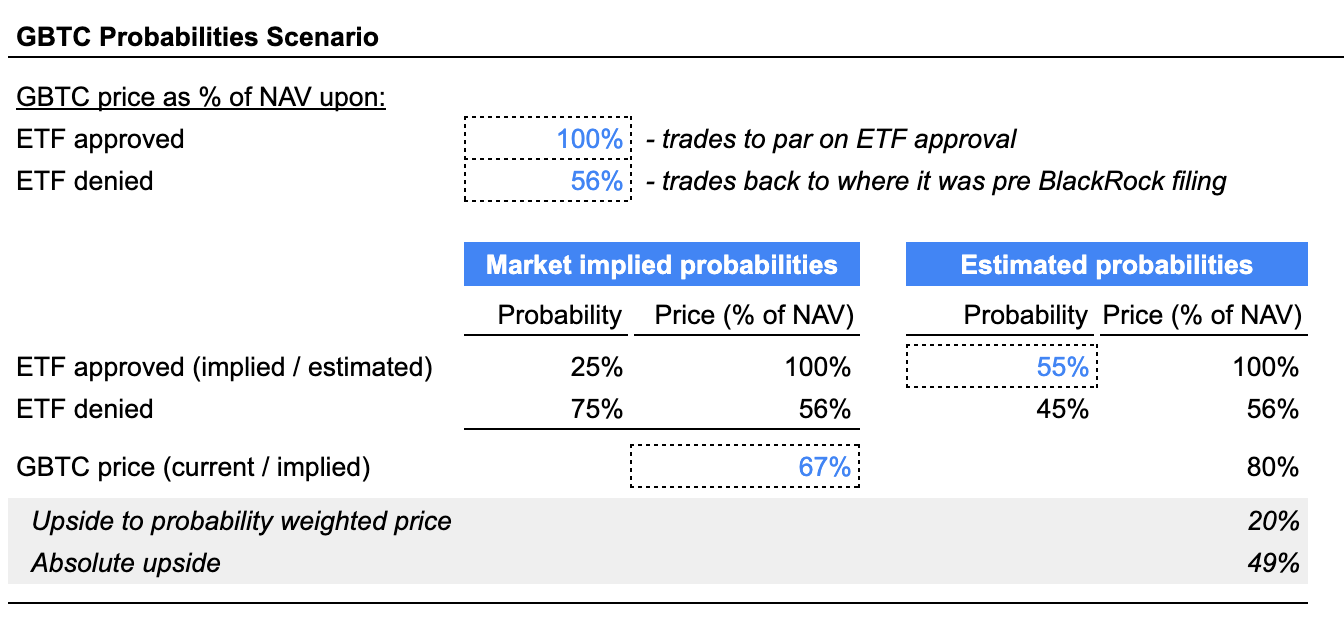

The GBTC discount has rallied 19% on the news. The discount has tightened from 44% to 33% (see table below).

GBTC is currently priced at 67% of NAV. Assuming GBTC trades to 100% of NAV upon any successful spot BTC ETF approval and to 56% on denial, then the market is pricing in a 25% probability of approval. If the chances are more like 55/45 approval/denial then GBTC should be trading at 80% of NAV, a 20% upside from the current GBTC price. If a spot BTC ETF is approved, GBTC should trade to 100% of NAV, a 49% upside. The table below outlines the calculations.

A path to listing a spot BTC ETF also means Grayscale’s fees will drastically compress. Grayscale charges a 2% management fee, whereas ETFs charge 0.5%-0.75%.

5. The impact on BTC is anyone’s guess, but here are some thoughts

The potential buying demand from a spot BTC ETF seems large. An ETF makes buying the asset much easier and helps legitimize it. There is conceivably lots of capital that was previously sitting on the sidelines that will now get into the market. Quantifying what the impact is hard.

GLD, the gold ETF, was the largest ETF launch. It raised $2 billion in a couple days when it launched in 2004. The market cap of gold at the time was $1 trillion. The immediate gold ETF buying demand represented 0.2% of the overall gold spot market value. If the same happened on a successful spot BTC ETF launch, then there could be $1.2 billion ($600 billion market cap x 0.2%) of BTC buying on the ETF launch. $4 billion worth of BTC trades on an average day. An incremental $1.2 billion isn’t going to move the needle that much. For context, on June 21, 2023 when BTC rallied 15%, $11 billion worth of BTC traded, an incremental $7 billion compared to the average volume. And it’s easier to buy BTC today than it was to buy gold before the launch of the gold ETF.

The market cap of gold increased by 5x in the 4 years after the launch of the gold ETF. How much of a factor did the ETF play into the rise of gold? Who knows.

The precedent example suggests that a spot BTC ETF may not be as big of a deal near term as BTC bulls may expect. The gold ETF likely did help increase the size of the gold market in the subsequent years. It made gold easily accessible to all investors. The gold ETF did not “legitimize” an asset, like the spot BTC ETF would. It only made it easier to buy. Estimating the near term impact is anyone’s guess. Longer term, it’s hard to see how a spot BTC ETF isn’t bullish…but how much? Wait and see.

One reason we may not have to wait that long: the Bitcoin halvening. A spot BTC ETF could be approved by mid February. The halvening is expected in mid April. The two coinciding could have a magnified impact on BTC price.

Stay curious.

My views expressed in this article were informed by Craig Salm, Eric Balchunas, James Seyffart and Austin Campbell. Thank you.

Don’t forget to hit the “♡ Like” button!

♡ are a big deal. They serve as a proxy for new visitors and feed into Substack’s algorithm that distributes my articles to all Substack readers.

And…why not share this article?

Follow me on Twitter @samuelmandrew for my latest takes.

Clarified a lot my questions. Well done review of the situation. Question I have. How much of available gold was in the LSE and other gold market reserves, available for sale vs. BTC. I don't think whales will be offering up more Comments?