The Future is NEAR

Investment Case for Near

Near is an emerging Layer 1 blockchain with a unique design architecture and an undervalued token. Near has essentially executed the original Ethereum 2.0 roadmap. The Near token has attractive economics and trades at 2x its treasury value. Near is the least well known best tech. The foundation has taken steps to address this shortcoming.

The tenets of Near’s investment thesis are:

Multichain world

Near delivered the original Ethereum 2.0 roadmap

Traction will catch up to tech

Restructured foundation setup to drive adoption

I elaborate on the investment case, triangulate Near valuation and explain what needs to happen to unlock its value.

Investment case:

1. Multichain world

Near has the potential to become a niche or dominant chain in a multichain world. Ethereum has cemented itself as the dominant programmable blockchain. Its network effects nearly enshrine its pole position. There is space for a handful of chains, likely consisting of one or two dominant chains and a few other niche chains. At this early stage, Near becoming a niche or dominant chain would crown it a success.

Over a thousand different blockchains exist today. There will be a handful of leading blockchains that dominate the market. Two opposing forces; preference and functionality, suggest there will be more than one blockchain and far less than a thousand.

Different users and applications prioritize different blockchain attributes; security, cost, speed, throughput, decentralization and functionality. Users will interact with and applications will be built on chains that best fit their own hierarchy of priorities. The hierarchy of priorities changes across different users. Choice is a good thing. Preferences for different attributes means there will be more than one dominant chain.

Functionality suggests activity will converge around a small number of chains. There are over 7,000 spoken languages and 180 fiat currencies in the world. Nearly all of commerce is conducted in three languages: English, Spanish and Chinese. Most commerce is conducted in US Dollar, Euro or Renminbi. Most of the world operates on the metric system, Greenwich Mean Time and the Gregorian calendar. The standard form to transport goods is the Twenty-foot Equivalent Unit. It’s a standardized metric to facilitate shipping goods by truck, train, ship and aircraft. If everyone conducted commerce in different languages, using different currencies, calendars and time and shipped goods of different sizes commerce would grind to a halt. It would be unnecessarily complicated. Simplified widely adopted standards facilitate functionality. Thousands, even hundreds, of blockchains hamper common standards. The world will coalesce around a few chains that balance enough preferences for its users and applications while ensuring functionality.

2. Near delivered the original Ethereum 2.0 roadmap

Near was founded in 2017 and its mainnet launched in April 2020. Its architecture was designed from the outset to deliver the original Ethereum 2.0 roadmap; namely scale through sharding. Near is the only blockchain that has successfully shipped sharding. Its transactions per second are, in theory, uncapped. Transactions costs are about ⅓ of a cent.

Sharding is a database concept applied to blockchain design. Databases, like blockchains, become cumbersome, slow and costly to run as they grow in size. Sharding is a way of partitioning a database into smaller pieces called shards. Most blockchains require every node to store all the information on chain and process all transactions. It makes for a secure chain, but a slow one.

Sharding allows for the blockchain to be secure, fast and scalable. It partitions the blockchain into smaller pieces and stores the data on different machines. Nodes are divided into smaller groups responsible for one part of the chain’s data. These individual groups can process transactions at the same time. Instead of one person verifying the transactions in one block, there are several people validating transactions in multiple blocks. The more shards, the faster the network. There is no limit to how many transactions can be processed because additional shards can continually be added.

Nightshade is Near’s sharding mechanism. There are four phases. The initial phase launched in November 2021. It sharded the state, but not the processing. The state was sharded into four parts. Validators needed to track all shards to ensure security. The second upgrade went live in September 2022, nine months after its original deadline. It introduced chunk-only producers. Each shard produces its own batch of data called a chunk. Chunks from different shards are added together to create a block. All the blocks are chained together on one Near blockchain. Chunk-only producers validate the chunks of their respective shard. It requires minimal computing power. Anyone can be a chunk-only producer. Chunk-only producers enable decentralization. The third phase implements fully sharded state and processing. Once completed, there will be a fully functional sharded mainnet with a fixed number of shards. Validators no longer need to track all shards. This phase has not yet been implemented. Launch timing is unclear. It’s speculated for sometime in 2023. The original launch was slated for Q3 2022. The final phase introduces dynamic resharding. Dynamic resharding adjusts the number of shards based on network demand. Additional shards are added when demand spikes and removed when they’re not needed. Dynamic resharding enables Near to cope with high throughput, yet not be saddled with the additional cost of spare capacity when it’s not needed.

The benefits of Near’s design are:

Fast finality: 1-2 second finality.

Uncapped scaling: Additional shards can be added uncapping the theoretical transaction throughput.

Independent scaling: Near is not reliant on Layer 2 scaling solutions and bridges between chains.

Ethereum did not scrap its original sharding roadmap because sharding is a bad idea. Ethereum was so far behind on its roadmap, it opted for rollups instead of sharding. Sharding would have required redesigning the Ethereum architecture. Near is not saddled with Ethereum’s technical debt. It’s able to execute sharding from the outset.

3. Traction will catch up to tech

Near is accessible to users and developers. It positions itself as the bridge from web2 to web3. Near designed appealing features for both users and developers.

For developers:

i) Programming language

Near is the only blockchain where smart-contracts can be written in Javascript and Rust. Javascript is by far the most common programming language. There are 14 million Javascript developers worldwide. Solidity and Rust are common blockchain programming languages. There are an estimated 200,000 and 3 million Solidity and Rust developers respectively. Developing on Near does not require learning a new programming language. Near appeals to the largest set of existing developers.

ii) Aurora EVM

Aurora is an Ethereum Virtual Machine implemented as a smart contract on Near. It allows Ethereum smart contracts to be executed on Near. It enables Ethereum applications to be easily redeployed on Near and benefit from Near’s lower transaction costs and faster transaction processing.

iii) Private shards

Enterprises can build private shards that are connected to Near’s public blockchain. Private shards are designed to meet the specific needs of the enterprise, without requiring it to build its own chain. Public chain contracts can call into private shard contracts and vice versa. Private shards are a potential path for enterprise adoption of public chains.

iv) Tokenomic developer incentive

30% of the gas fee for transactions involving a smart contract is paid to the developer of the smart contract. It’s a form of royalty for the developers. The more useful the smart contract is, the more it is used, the more will be earned by the developer.

For users:

i) Blockchain Operating System

Near launched the Blockchain Operating System (“BOS”) in March 2023. BOS enables users to navigate, what Near calls, the Open Web. The Open Web allows users to control their identity, assets and data. BOS is a common layer for browsing and discovering Open Web applications across all blockchains. Crypto user onboarding is disjointed and unorganized. BOS brings together all applications across all chains in one place to simplify users discovery and onboarding experience.

ii) Meta transactions

Near implemented meta transactions at the end of 2022. Meta transactions allow third parties to initiate and pay the transaction fees on behalf of a user account. Users need to buy a blockchain’s native token in order to interact with anything on chain. Users need to pay before they use it. That’s uncommon for new products. It’s a massive hurdle to onboarding users. Meta transactions remove that hurdle.

iii) Account abstraction

Near has built in account abstraction. Near users need to create a Near account. Accounts have unique features:

Human readable accounts: accounts have addresses like sam.near instead of long strings of characters.

Multiple permissioned keys: Near accounts have multiple keys each with their own permissions. Account holders can grant different access to third parties and revoke them at any time.

Smart contract enabled: Near accounts are smart contract enabled. Developers can create account specific smart contracts in Javascript or Rust.

Mutable state: Near accounts have state storage, which can change when the account’s smart contract performs a transaction.

These features differentiate Near Accounts from Ethereum Wallets. Ethereum account abstraction are innovations that convert Ethereum Wallets into programmable smart contracts. These innovations make for better user experiences. Near was designed with account abstraction in mind.

iv) Attractive tokenomics

Value created on chain accrues to Near token holders via Near’s burn mechanism. Nearly all Near fees are burned. For transactions involving a smart contract, 30% of fees are distributed to the smart contract developer and 70% are burned. 100% of the fees are burned in transactions that don’t involve smart contracts.

Gas fees are not used to pay validators. Validators are paid in new token issuance. Token inflation is capped at 5% per year. As transaction volume increases, the burn mechanism offsets token inflation rendering Near net deflationary at high transaction volumes. For example, at 1 billion transactions per day, Near’s net inflation is 1.35% and at 1.5 billion per day token supply is reduced by 0.5% per year.

Traction is growing

i) Daily active addresses and transactions

Near has roughly 50,000 daily active addresses. Its active users have grown 2.5x in a year. Most chains experienced flat to declining user growth trends, with the exception of Polygon that grew daily active users by 20%. Near’s growth spike in September 2022 was driven by the launch of Sweat Economy. Sweat is a web2 move-to-earn app with 90 million users. It created a blockchain enabled version of its app on Near. Sweat converted some of its existing web2 users into on chain users and grew Near daily active users by 16x overnight. Sweat was a one-time growth event. Without it Near’s user growth would have likely trended like other chains. Successfully integrating such a large inflow of users bodes well for Near’s technology.

In the last year growth in daily transactions has varied across prominent L1s. Solana grew 25%, Polygon declined 25%, Ethereum was flat and Avalanche grew 100%. Near’s daily transactions have hovered around 500k per day since summer of 2022. But are down from an average of 750k in the spring of 2022. Near’s peak average daily transaction was 2 million. Near’s 35% peak to current decline is not abnormal. Solana’s peak decline to today is 50%, Polygon’s is 60% and Ethereum is 20%.

ii) Developers

Electric Capital’s Developer Report highlights that major ecosystems are emerging beyond Bitcoin and Ethereum. 72% of monthly active developers work outside the Bitcoin and Ethereum ecosystems. Solana, NEAR, and Polygon grew 40% year-over-year in December and have 500+ total monthly active developers. That bodes well for Near. However, Near’s developer count has recently underperformed its peers.

iii) Benchmarking

Near favorably benchmarks to its competitors. Near’s fully diluted market cap is about 20% of its peer average (excluding Bitcoin and Ethereum). Yet Near has +120% of Avalanche, Cosmos and Aptos DAUs (and ~20% of Polygon and Solana). Daily transactions comparison is a mixed read. Near’s developer numbers are nearly the same or higher than its competitors. Where Near does not stack up well is TVL. Near has a much smaller TVL than its peers. On all other metrics, Near comps well to its peers, yet has a significantly smaller fully diluted market cap.

4. Restructured foundation

Near restructured its foundation in June 2022. A whole new team has been brought in starting with hiring Circle veteran Marieke Flament as CEO in December 2021. Near scrapped its funding program in November 2022. Near is pursuing a diligent approach to deploy capital and support projects that best serve the ecosystem.

Business development has been Near’s shortcoming. For arguably some of the best tech in the market and decent relative metrics, Near punches well below its weight class. Near Foundation seems to be aware of that.

The retooled foundation publishes quarterly reports reminiscent of reports from growth-stage companies. OKRs are disclosed, discussed and tracked. It remains to be seen if the foundation can build an ecosystem to rival others. The reorganized foundation is a step in the right direction.

Valuation

Near’s valuation is straightforward and largely misunderstood. There are three compelling valuation angles for Near.

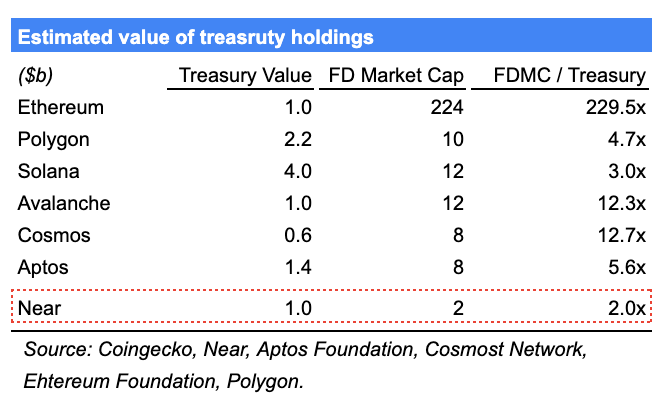

i) Treasury multiple

Near trades at 2x the value of money it has on hand. The market is implying that Near will deliver a 2x return on the capital it has to deploy. Near has $1 billion in its treasury to develop its ecosystem. It has a $2 billion fully diluted market cap. Between Near’s tech, decent traction, focus on user and developer accessibility and restructured foundation, I think it will deliver more than a 2x return.

Near competitors trade at much higher treasury value multiples (see table below).

Treasury value captures the amount of capital a protocol has to invest in developing its ecosystem. For the purposes of this analysis, it includes capital earmarked for protocol foundations, community and grants.

Treasury figures are not regularly disclosed. Notwithstanding crypto’s machination with ‘transparency.’ Near is the only protocol that discloses its treasury capital on a quarterly basis. Ethereum’s treasury value was last disclosed in March 2022. The table above adjusts the March 2022 figure for today’s ETH price. Polygon disclosed its treasury value February 2023. The treasury value for the other chains is estimated by determining the current allocation of tokens to foundation, community and grants. These figures, with the exception of Near, likely all overstate the treasury value. They do not account for disbursements made to operate the foundation and invest in the ecosystem. Therefore, the multiples for Near’s competitors are likely higher than indicated in the table above.

ii) Ethereum relative value

Near trades at 0.9% of Ethereum’s market cap, down from 3% a year ago and 1.8% pre-FTX. The market has buoyed ETH on the back of a store of value thesis in the wake of recent banking crises and money printing concerns. Near should not benefit from a similar dynamic. However, Near’s competitors trade on average at nearly 5% of Ethereum’s market cap.

Near should not trade at 5% of Ethereum, but it should trade higher than 0.9%. Near’s benchmarked metrics (see Benchmark Analysis table further up) comp well to its peers. That alone should have Near trading at 2-3% Ethereum market cap.

The one metric Near comps poorly on is TVL. I suspect that is what is dragging Near’s relative value compared to its peers.

iii) Near fundraise price

Near raised $500 million at the peak of the market. In January 2022, Near raised $150 million from a16z, Dragonfly and others. In April 2022, Near raised $350 million led by Tiger Global. The Near token price was about $14 at the time of the raises. It has fallen 85% to $2 since then.

Near is in a better position today than it was at the time of the raises. The bear market is more advantageous for Near than its competitors. Users and applications were mercenaries in the bull market. They went to whatever chain paid them to transact and build. Competitors were flush with cash to buy users. Those days are over. Competition in the bear market is based on tech capability and support the foundation can provide. Near can better compete now because i) its performant tech, ii) its capital position relative to peers has improved and iii) the reorganized foundation is better equipped to help the ecosystem.

What needs to happen?

Near needs to do two things to unlock its value.

i) Execute on BD

Near’s weakness has been its business development. It’s not top of mind for developers. I’m optimistic the reorganized foundation can address this. They need a game plan for where and how to compete to drive user and transaction growth. Since Near is trading at 2x its treasury value, you nearly have a free option on the foundation’s ability to execute. Plus, Near is arguably cheap relative to its peers. There could be a valuation uplift on a relative value basis alone.

You’re not paying much today for Near’s potential. So if Near doesn’t execute, I don’t think you’ll lose much.

ii) Ship Nightshade

Near needs to ship phase 3 of Nightshade. It’s the last step in implementing a fully sharded state and processing. It’s a big deal in demonstrating the strength of Near’s tech. The original launch was slated for Q3 2022. There is no update on when it will go live. Near should provide one.

Stay curious.

Please reach out with any feedback or challenges of my assessment of Near.

curious if multiversX came up in your research, have a similar sharding approach and adoption has also been limited to date. any thoughts on how the two compare?