Silicon Valley Bank (“SVB”) entered receivership on Friday, March 10, 2023. The Federal Deposit Insurance Corporation (“FDIC”) is the receiver. The FDIC now operates SVB. Insured depositors can get their deposits on Monday. Uninsured depositors will get paid an advance dividend in the next few weeks. Uninsured depositors will receive a receivership certificate for the remaining amount of their uninsured deposits.

It’s bad…like real bad.

SVB is one of the 20 largest commercial banks in the US. It’s the second largest collapse of a US financial institution in history.

SVB is likely insolvent and was facing a bank run. SVB had $173 billion of customer deposits and $211 billion of assets as of 12/31/22.

The issue is that $164 billion of its assets are not worth what they’re recorded at on their 12/31/22 balance sheet. $91 billion of its assets are accounted for as ‘held-to-maturity securities.’ They’re accounted for at the cost they were originally bought for. These are rate sensitive credit securities. Their value had declined as rates increased. $74 billion of assets are loans SVB made. These loans were made to the tech industry in boon times. It’s unlikely these loans are all repaid at par at maturity. SVB’s liabilities are now larger than its assets.

Depositors panicked and started pulling money from SVB. A bank run ensued. The California Department of Financial Protection and Innovation closed SVB and placed it into receivership. The FDIC will orchestrate the unwind and/or sale of SVB. The proceeds will be used to repay depositors and creditors. The equity value is zero. Depositors may lose part of the deposits they had at the bank.

Losing customer deposits is a HUGE deal. It risks sparking a bank run on other banks. Fearing the worst, depositors start indiscriminately withdrawing their money. The cycle feeds itself and compounds. The first to withdraw gets their money back, the last gets nothing.

The failure of SVB has a specific impact on crypto. SVB holds $3.3 billion of USD deposits that backs USDC. Late Friday night eastern standard, USDC broke its peg. The market is worried USDC is in fact not backed 1:1 by USD.

Asset backed stablecoins are one of crypto’s foremost innovations. They’re a digital representation of an actual dollar. They facilitate transferring USD globally at low cost and with instantaneous settlement. People trust them because their value is stable and they’re backed by actual USD cash and equivalents.

All of a sudden, USDC, the second largest stablecoin with $44 billion in circulation prior to the SVB debacle, may no longer be backed 1:1.

That’s a big problem.

If a digital dollar is not backed by an actual dollar. Then why do I own it? I certainly wouldn’t ascribe $1 value to it. Panic selling ensues to get out of the digital dollar into real dollars. Knock on effects ripple through crypto markets.

But that hasn’t happened.

USDC in circulation has dropped from $44 billion Friday afternoon to $37 billion Saturday morning EST. The peg is somewhat stable at 90 cents/dollar.

I believe that’s because things are not that dire for Circle, the issuer of USDC. The potential loses Circle may incur on its USD deposits at SVB are ~$500 million. Circle has other means of backfilling compromised deposits.

There are four ways things could play out favorably for Circle/USDC:

Favorable SVB deposit recovery

SVB is acquired

Circle Internet Finance steps in

Strategic Circle investor steps in

Brought to you by FRNT.

FRNT is a leading crypto investment bank. It’s also the author of the best crypto daily note. I’ve been a daily reader for over 3 years. Subscribe to get distilled insightful crypto daily news.

1. Favorable SVB deposit recovery

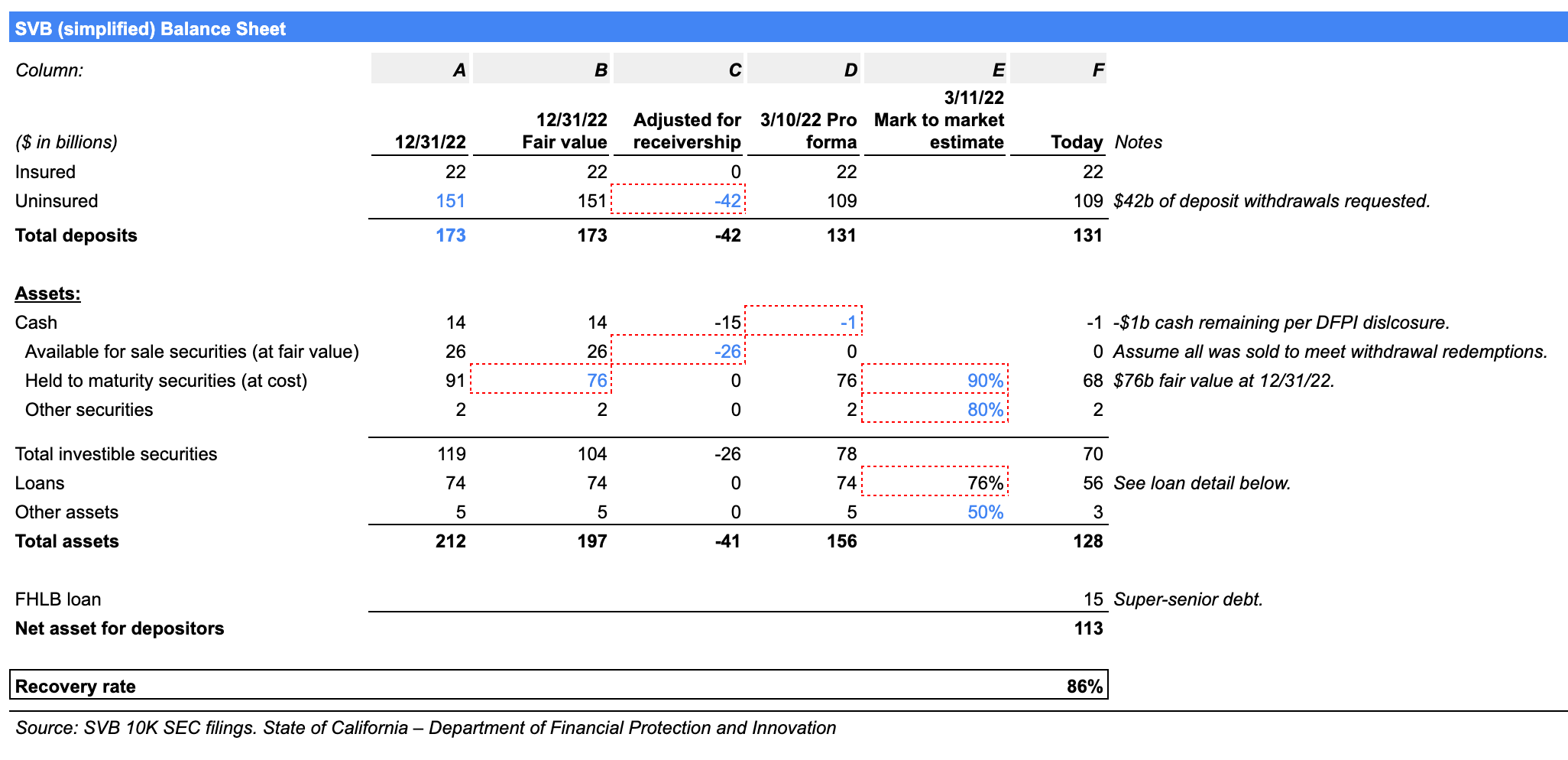

SVB deposits are likely worth 86 cents/dollar. The recovery rate (ie 86 cents/dollar) is calculated by dividing SVB’s estimated asset value by its deposits. The biggest driver of the drop in asset value from $212 billion on 12/31/22 to today’s value is i) the large deposit withdrawals and accompanying asset sales this past week, ii) the value ascribed to ‘held to maturity securities’ and iii) ‘loans.’

I estimate ‘held to maturity securities’ are worth 75% of their book value. $86 billion of the $91 billion are in securities that have a maturity in over 10 years. $57 billion of the $86 billion is invested in mortgage backed securities. SVB 10K filing states that the fair market value as of 12/31/22 of the $91 billion of ‘held to maturity securities’ is $76 billion. I assume an additional 10% hair cut from the 12/31/22 fair market value.

I estimate the ‘loans’ are worth 76% of their book value. The loan portfolio will be sold. The credit is probably better than most people think. The discount is due to having to sell it quickly. The detail of the loan portfolio is broken down in a chart further below.

The table immediately below summarizes the balance sheet, how things have moved from 12/31/22 to today and the key assumptions to imply depositor recovery rate. The table starts with the reported balance sheet on 12/31/22, column A. Column B adjusts the ‘held to maturity securities’ to their far value as of 12/31/22. Column C are the adjustments to the 12/31/22 Fair Value balance sheet. They include $42 billion of deposit withdrawals on March 9, 2023 and a negative cash balance of $1 billion. I assume the ‘available for sale securities’ were sold to fund this withdrawals. Column D shows the pro-forma balance sheet as of 3/10/22. Column E highlight the additional mark to market estimate of what the assets could be worth. Column F is the balance sheet today. It encapsulates the up to date deposit figure and my estimate on what the assets are worth. The total estimated value of assets of $128 billion is reduced by $15 billion of super-senior debt from the Federal Home Loan Bank program (FHLB). This debt is repaid before depositors.

Below is the breakdown of SVB loan portfolio.

I’ve made simplifying assumptions. The insured deposits will get 100 cents/dollar. In these calculations I’ve treated depositors the same. This simplifying assumption could impact uninsured depositors by ~1 cent/dollar. Circle USD and equivalent reserve balance backing USDC was $100 million larger than the total USDC in circulation as of March 9, 2023. That would increase recovery by ~0.5 cents/dollar.

Circle has $3.3 billion of deposits at SVB. At an 86% recovery rate, Circle could lose ~$500 million worth of its USD deposits held at SVB.

The market is pricing in a $3.7 billion deposit loss for Circle. $37 billion USDC is in circulation trading at 90 cents/dollar ($37b x 10% = $3.7b). That seems too punitive. I’ll come back to this later.

Circle has other ways to backfill the compromised ~$500 million worth USD deposits at SBV. Even if my assumptions are off, Circle has is in good standing. The following outcomes explain how that could work.

2. SVB is acquired

SVB will likely be acquired before Monday morning when financial markets reopen. If SVB is acquired, all depositors would almost certainly get 100 cents/dollar. The new buyer would be on the hook for SVB’s deposits.

SVB will likely be acquired because:

Precedent: SVB imploding and losing customer deposits sets a bad precedent that depositors’ money is not safe at US banks. The financial system is based on trust. If that trust disappears, we’re in for a lot more trouble. It’s one thing if equity holders and creditors are wiped out. In the case of SVB, they should be. It’s a whole other thing for depositors lose their money.

Avoid contagion: A bank run on other banks could be triggered if SVB depositors lose their money. Widespread contagion the likes of 2008 would send shockwaves through the financial system. The stakes are too high to let this happen.

Government financing: I believe the government would provide favorable financing to a buyer to ensure depositors are made whole. The funding amount is minuscule relative to the US government trillion dollar budgets. SVB needs ~$20 billion to ensure depositors are made whole ($173b in deposits - $152b of market-to-market assets).

Attractive takeover: SVB is a top 20 commercial bank in the US by deposits. The top 5 banks have >$1 trillion of deposits each. The next 15 have several hundred billion each. Acquiring SVB on favorable terms could be a way for another top 20 bank to significantly grow its deposit base.

Technically, SVB will go through receivership, equity holders and creditors will be impaired and then the deposits will be taken over. But simplistically the concept is the same.

3. Circle Internet Finance steps in

Circle Internet Finance is Circle’s parent company. It had $493 million in cash on its balance sheet as at 6/30/22. This is cash that belongs to Circle Internet Finance. It is separate from the cash held in segregated accounts that backs USDC. The cash balance has fluctuated since 6/30/22. Funding on-going Circle operations reduced cash. Higher Circle revenue likely offset part of Circle’s operating costs since 6/30/22. Suffice it say, Circle has a few hundred million it could use to backfill whatever losses were incurred on its USD deposits at SVB.

4. Circle investor steps in

Circle operates an attractive business. Its revenue comes from the interest it earns on the $44 billion of deposits that back USDC. In today’s higher rate environment, Circle could earn 3% in safe liquid assets. 2 year US treasuries yield 4.5%. A blended return of 2% on $44 billion is $880m of revenue. Circle’s annual operating costs is roughly $500 million. As long as Circle has a large base of USDC in circulation, it makes a ton of money.

Circle would have no problem lining up a lender for a few hundred million to back fill the hole left by lost SVB deposits. Private equity and hedge funds would be lining up to lend money to Circle. Coinbase has $4.4 billion cash on its balance sheet. It could easily back fill Circle’s deposit loss.

Tying it all together…

SVB going down is bad. I believe that by Monday morning there will be a solution whereby depositors are made whole.

The knock on impact to Circle is a problem. But it is not an insurmountable one. There are feasible ways the potentially lost USD deposits backing USDC are restored. I believe crisis will be averted.

I estimate the potential loss of Circle’s USD held at SVB could be ~$500 million. There is a good chance through any one of i) SVB acquisition, ii) Circle Internet Finance or iii) a Circle investor that deposits backing USDC will return to 1:1 and the peg will go back to $1.

Circle does not have a solvency problem. It’ll likely get back most or all of SVB compromised deposits. Circle has a timing problem. It could take months to get the SVB deposits back. During that time, USDC in circulation could continue to drop. The more USDC in circulation declines, the more compromised Circle’s business becomes.

But…The crypto market is pricing in a $3.7 billion deposit loss for Circle. That means either i) the market is not understanding how things will play out or ii) the market is expecting further contagion to other banks where Circle has deposits. Circle banks with Bank of New York Mellon, Citizens Trust Bank, Customers Bank, New York Community Bank, Signature Bank and Silicon Valley Bank.

If the market is concerned with further contagion. Here is how to think about it. Circle has $32.4 billion in a short-dated US treasury portfolio managed by BlackRock. The portfolio is marked-to-market daily. It has not lost its value. The floor price of USDC is 75 cents/dollar. If Circle lost all its USD deposits held at various banks, it would be left with its short-dated US treasury portfolio that comprises $32.4 of the $43.4 billion in circulation (32.4 / 43.4 = 75%).

The price range of USDC should be 75-100 cents.

These events highlight how tied Circle is to the US financial system. Part of the benefit of USDC is that it is tied to the US financial system. A USD stablecoin is a unit of measure we all understand backed by an asset the world views as valuable. But USDC can’t operate without its ties to the US financial system. SVB highlighted that a combination of the bank’s asset management and fast rate hikes from the Fed can flip a bank upside down undermining the sanctity of a USD backed stablecoin. In this case, however, Circle has options to reaffirm USDC reserve integrity.

Stay tuned. If SVB is not sealed off and contagion spreads to other banks, all bets are off. It’s going to get ugly.

Excellent thought process. It does make sense for the government to step in to prevent contagion, but they did not do it this early in the GFC. Your point about equity holders and creditors vs depositors is a key difference. And this bank is something of a lifeblood for a key segment of our productive economy.