DeFi Death?

A sober assessment of DeFi; is this stuff actually valuable?

Is Decentralized Finance (“DeFi”) dead?

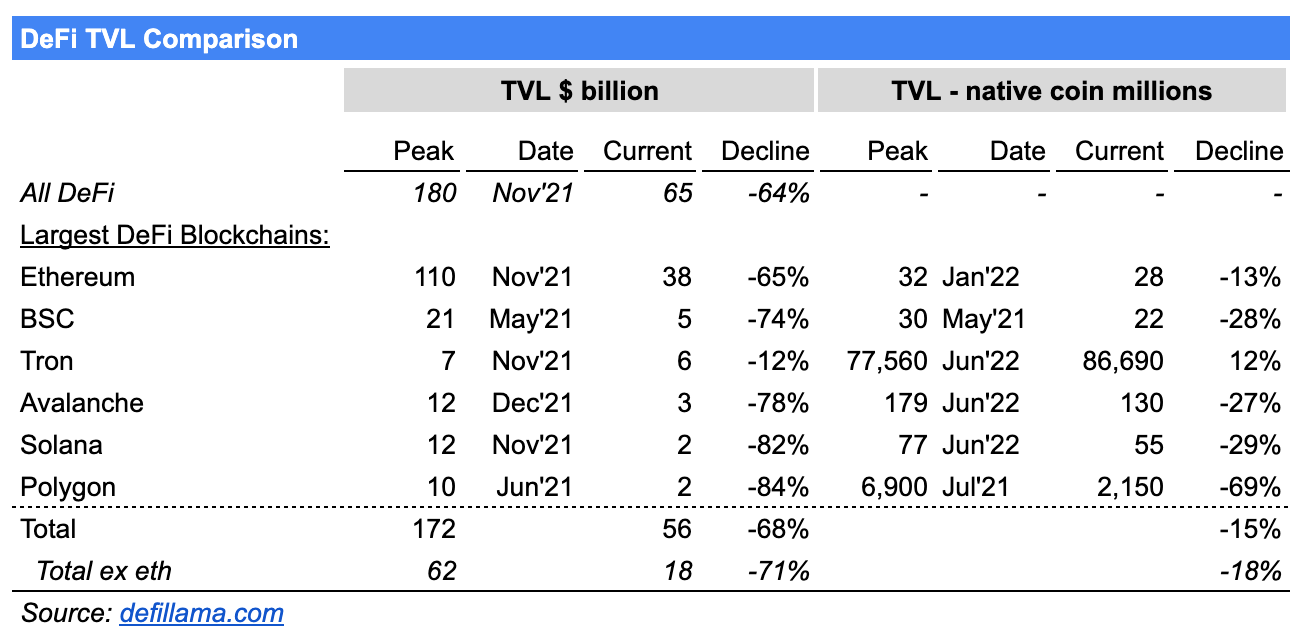

The Total Valued Locked (“TVL”), a measure in dollars of the value of all digital assets deposited on DeFi protocols, has dropped nearly 65% to $65 billion.

The Wall Street Journal noted:

“DeFi has ended up committing all the same sins as Wall Street, essentially becoming a vehicle for a new generation to engage in the rampant speculation typical of pre-2008 investment bankers.”

It’s mocked in pop culture.

In this piece I explain:

Actually, DeFi ain’t dead

Okay, it’s not dead - so what is it?

So, is there anything actually valuable in DeFi?

Outlook for DeFi

Actually, DeFi ain’t dead

TVL is misleading. DeFi and Centralized Finance (“CeFi) are conflated. And the mockery, well that happens. Let’s take one at a time.

TVL

The majority of DeFi activity occurs on the Ethereum blockchain. $38 billion of $65 billion total DeFi TVL is in protocols running on Ethereum. DeFi TVL on the Ethereum blockchain is down to $38 billion from a peak of $110 billion, a 65% decline. But the amount of eth in DeFi TVL remains near an all time high of 28 million eth tokens. People have not removed their eth from DeFi. It’s just worth a lot less in USD terms.

The same trend holds for DeFi TVL of the next largest blockchains. Dollar denominated TVL is -68%. Native coin TVL is -15%. People are not pulling their digital assets from DeFi protocols. It’s not dead.

DeFi vs CeFi

CeFi has been conflated with DeFi. The WSJ article and others have made that error. Several CeFi platforms imploded by “committing all the same sins as Wall Street.” I explained their inner workings and downfall in CeFi Casualties.

Celsius, BlockFi, Voyager and a handful of CeFi platforms took depositors’ savings and promised them high returns. They lent the deposits without proper loan underwriting and woeful disregard of basic risk management. It was similar to “pre-2008 investment bankers.” They are now insolvent. Depositors lost their savings.

CeFi platforms have little to do with blockchain technology. They just happen to transact in crypto. Their infrastructure is the same as TradFi. Their procedures are inferior to TradFi. They are not held to the same regulatory standards. It’s the worst of TradFi masquerading as a “Web3” version of itself.

DeFi protocols have uncompromising procedures and robust infrastructure. During the market turmoil, DeFi protocols operated exactly as they are meant to. Withdrawals were not halted. Service did not stop. Loans were issued and repaid. It was business as usual. DeFi lending protocols and Terra/Luna serve as examples.

DeFi lending protocols

DeFi lending protocols are governed by the rules established by their community and imbued in the smart contracts that govern how loans are issued, collateralized and repaid. There is no ambiguity. No preferential treatment. If the requirements are not met, no loan is issued. If risk thresholds are breached, the collateral is automatically sold and the loan repaid.

The combined loan books of Compound, Aave and Maker is an estimated $12 billion. All had loans to 3AC or similar operators. All remain solvent.

All transactions are recorded on chain. Activity is transparent in real time. The size of the loan, liquidation price, collateral and borrower address is all visible on tools like Maker Risk.

Terra/Luna

Contrary to popular belief, Terra/Luna is a validation of DeFi. Terra was a DeFi protocol that developed an algorithmic stablecoin US Terra. As explained in WTF LFG…crypto crash explained, it lost its peg and destroyed $40 billion of market cap in four days. Terra serves as an example of smart contracts executing as they are meant to. The Terra code was visible for everyone to see. Few bothered to understand how it worked. When US Terra traded below its $1 peg, smart contracts automatically minted new Luna in increasing amounts to restore the dwindling peg. A set of visible, auditable and incorruptible mathematical equations set out what would happen if the peg broke. Although the peg was not restored, the code executed exactly as it intended. It was an error in logic, not smart contracts.

Laughing stock

Volatile prices, frauds and hacks make crypto a punching bag. The lack of education of the wider public is not the public’s fault. It’s crypto’s fault.

David Letterman ridiculed Bill Gates’ description of the internet in 1995. Letterman quips “uhhh…does radio ring a bell?” in response to Gates’ example that you could use the internet to listen to a baseball game.

The point is not that crypto will follow the internet’s success. It may or may not. The point is innovation gets ridiculed.

“First they ignore you, then they laugh at you, then they fight you.”

Crypto is wedged between the laugh and fight stage.

Okay, it’s not dead - so what is it?

Decentralized Finance (“DeFi”) is a crypto term used to define financial services, such as lending, borrowing and trading, provided through blockchain protocols. The services are “decentralized” because no centralized governing authority is required to approve a loan, receive a deposit or execute a trade. Smart contracts govern how services are rendered.

DeFi is primarily used for:

Credit (borrowing & lending)

Trading

The biggest DeFi protocols by market cap and TVL provide lending, borrowing and trading.

Maker, Aave and Uniswap exemplify the innovative technology DeFi has developed.

Maker

Maker is a borrowing platform powered by its stablecoin Dai, which is pegged to $1. Dai is minted in the form of a new loan, when a borrower provides crypto assets as collateral. Maker provides overcollateralized loans, meaning the value of the collateral is worth more than the loan. For example, a borrower provides $150 of eth to get a $100 Dai loan. Unlike TradFi, there is no central authority governing the terms, underwriting and enforcement of the Maker loan. Smart contracts govern the loan. Anyone who provides the necessary collateral can get a loan instantaneously. If the predetermined liquidation price (i.e. the price at which the underlying collateral breaches the minimum collateralization ratio) is triggered, the collateral is automatically sold and the loan is repaid.

Aave

Aave is a borrowing and lending pool. Like Maker, Aave provides overcollateralized loans. Aave pools together depositor assets. Depositors deposit crypto on Aave to earn a yield. Loans are issued to borrowers from the pool of crypto assets deposited. No central governing authority exists. Smart contracts dictate collateralization ratios, execute forced liquidation if the collateral value declines, and sets lending and borrowing rates. Aave is the evolution from peer-to-peer lending to pool-to-peer lending.

Uniswap

Uniswap is a decentralized exchange used to trade digital assets. Uniswap uses an Automated Market Maker (“AMM”) instead of central limit order books. TradFi uses order books to match buyers and sellers. AMMs work by trading with a liquidity pool instead of discrete buyer or seller. Liquidity providers contribute an asset pair, such as an equal amount of btc/eth, to a liquidity pool in exchange for receiving part of the trade execution fees.

So, is there anything actually valuable in DeFi?

DeFi is used for credit and trading. Let’s break down what that is.

The benefit of credit

Credit is valuable. It powers economic growth. A family buys a home with a mortgage. An entrepreneur gets a business loan to open a store. A business expands its facility using a bank loan. Apple issues a billion dollar bond to fund research and development. The US government issues treasury bonds to fund its budget. In each case, new money is created to fund something with an expected economic benefit.

If individuals, companies and countries only relied on the cash they had on hand or selling equity, growth would be much slower. Total credit issuance (excluding government debt) in the US in 2021 topped $12 trillion. Total equity issuance in the US in 2021 was $436 billion. Credit drives the economy.

DeFi Credit

DeFi credit is not as valuable as TradFi credit. Businesses do not use DeFi credit to fund their growth. DeFi credit is inefficient capital. Overcollateralization makes DeFi lending and borrowing protocols robust. It is why they are all solvent, while CeFi counterparts are not. It also makes DeFi loans untenable for businesses.

For example, if a business needs to provide $150 worth of crypto collateral for a $100 loan, it is more efficient for it to use the $150.

DeFi loans are used for trading margin loans. Unlike a business, crypto trading firm have digital assets to use as collateral. It’s an efficient use of capital for them because the capital can be recycled over and over again to create an even larger position.

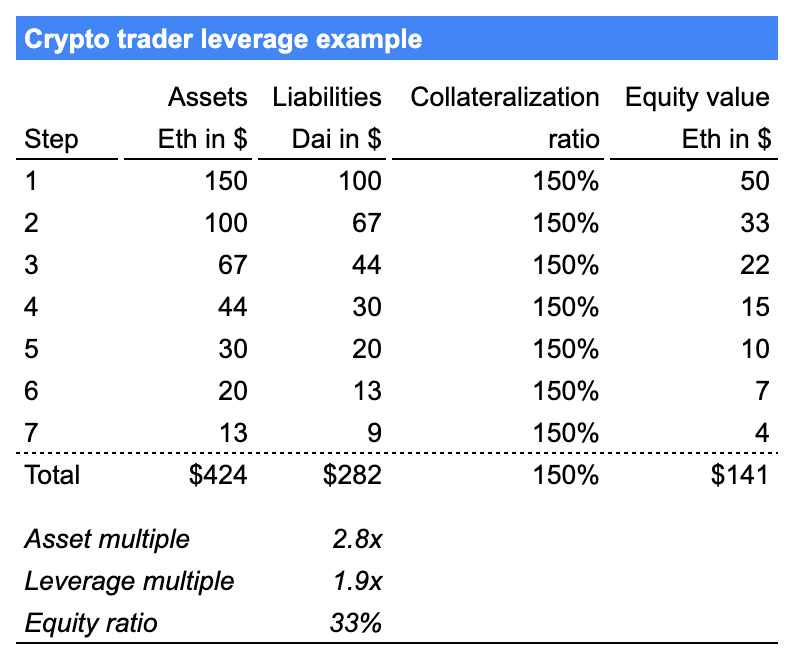

For example, I own $150 worth of eth. I then use the $150 of eth as collateral for a $100 stablecoin loan; that’s step 1. In step 2, I repeat step 1 with the new capital. I use the $100 of eth I just bought with the stablecoin loan as collateral for a new $67 stablecoin loan. Step 3, I use the $67 stablecoin loan to buy $67 worth of eth. I repeat that over and over again. The table below illustrates repeating it seven times.

The outcome is turning $150 worth of eth into $424 worth of eth. I’ve incurred $282 worth of stablecoin loans for an equity value of $141. It’s capital efficient because I’ve grown my eth exposure 2.8x without deploying additional equity.

Stablecoin loans collateralized by eth incurred interest of ~2% (5-10% at times). A trader is happy to pay 2-10% borrow cost when eth prices are growing 400% per year as they did from 2019 to 2021 or when crypto yield protocols generate 20% APY. It’s called a carry trade. You borrow at a low rate to invest in higher yielding assets.

The trouble is when prices decline a wave of deleveraging sets in. The loan from the example above gets automatically liquidated at 135% collateralization ratio. If the price of eth falls 10% all my eth will be sold. The market experiences a $381 ($424 x -10%) sell pressure instead of $135 ($150 x -10%) sell pressure; that’s deleveraging in action. 2.8x the amount of eth is sold. On a much larger scale that’s what’s been happening in crypto markets.

DeFi loans have mostly been used as trading margin loans. They work well. They are innovative. But trading margin loans do not drive economic activity. They drive asset bubbles.

For DeFi loans to drive economic activity, they need to be attractive to businesses. They need to be under collateralized or collateralized by off-chain business assets. Either case requires a central authority. The former to underwrite the business specific risk of an under collateralized loan. Like a bank underwrites the cash flows and fixed assets of a borrower. The latter to sue the borrower and take possession of their assets if they default. Both cases seem unlikely to be executable by programmable smart contracts.

The benefit of trading

Markets enable participants to trade goods, services and assets. Financial markets specialize in trading assets. The value of an asset is what someone else is willing to pay for it. Markets pool potential buyers and sellers. They facilitate price discovery.

DeFi trading

Decentralized exchanges utilizing AMMs are ingenious. They provide liquidity without requiring discrete buyers and sellers transacting at the same price. Centralized order books require a middle-man facilitating the transactions and buyers and sellers transacting at the same price. AMMs provide more liquidity and a lower execution cost. AMMs could revolutionize financial markets.

Trading assets more efficiently does not create meaningful economic value. If financial securities could be traded more efficiently today, would that impact economic growth? It would lower friction costs. The savings from which could be redeployed into economic activity. But I doubt it would be a game changer.

DeFi outlook

DeFi has powered innovation for a new form of lending, borrowing and trading. It’s being used a lot. It’s working well. But so far the largest use cases are not creating economic value.

Why could it be valuable?

DeFi does two things:

Increases the speed of commerce

Increases the amount and velocity of currency

Facilitating instantaneous transactions, globally without pre-established counter-party trust increases the pace of commerce. Issuing loans instantly to whoever meets the preconditions increases the amount and velocity of currency in the crypto ecosystem.

Throughout history economic growth has been spurred by increasing speed of commerce and the amount and velocity of currency. The advent of a common medium of exchange, currency (i.e. money), accelerated commerce by facilitating trade of goods for money instead of bartering. In 14th century Italy, credit became prevalent. It funded the ambitious growth plans of businessmen and sovereign nations. Credit created more money. It allowed businesses and countries to grow beyond the means of their existing capital. The industrial revolution spirited global trade as goods could be shipped and money transferred globally. E-commerce hypercharged commerce allowing consumers to buy goods at the click of a button. Each successive evolution increased the speed of commerce and the amount and velocity of money in the system. It drove growth. DeFi protocols could be the next evolution.

What additional benefit will come from even faster commerce?

I don’t know. But I believe the millenia long trend will continue.

When broadband was developed in the early 2000s, people asked “why do I need a faster internet?” The internet was used to read static web pages and email. Faster speed didn’t help those functions. We did not see at the time that broadband would pave the way for e-commerce and streaming. Broadband revolutionized how we use the internet. It made the internet ubiquitous and accelerated commerce. DeFi may be in a similar position today.

Greenshoots

There are emerging pockets of DeFi that are creating economic value. A couple examples include:

Lending

Goldfinch provides uncollateralized crypto loans to off-chain businesses. Their innovative underwriting process provides borrowers with attractive loans and lenders with reasonable security. It addresses the shortcomings of DeFi loans previously described. Goldfinch has $100 million TVL. Up from $20 million in September when it launched. Its TVL in eth has grown 14x from 6,500 eth to 92,000. Goldfinch borrowers include Payjoy who provides smartphone financing in Mexico. Aspire who provides business financing in South East Asia. Quick Check who provides micro consumer loans in Nigeria.

Goldfinch borrowers outline the terms of their requested loan. Goldfinch auditors verify the legitimacy of the borrower in exchange for earning Goldfinch tokens. Goldfinch backers underwrite the loan. Backers provide first loss junior loan capital in exchange for higher returns. Goldfinch liquidity providers provide capital that is distributed across various loans as senior loan capital. Liquidity providers earn a lower return than backers. Backers can have off-chain legal agreements with the borrower. Borrowers, auditors, backers and liquidity providers can be anyone. Their behavior is incentivized by Goldfinch tokens.

High interest low collateral loans are useful in emerging markets where access to capital is poor. Goldfinch’s blockchain based application facilitates international lending.

Money transfers

Stablecoins, the non-algorithmic kind, create real economic value. They are akin to digital dollars, euros and other currencies. Stablecoins are an attractive store of value for people facing hyperinflation and asset confiscation. They enable instantaneous international transfers for fractions of a cent. Anyone with an internet connection and wallet can transact. No bank account is required.

There is $150 billion worth of stablecoins in circulation. The market is dominated by two players, Tether and Circle. There is $65 and $55 billion of USD Tether and USD Circle respectively in circulation. Circle has 1.5 million users in 190 countries that trade $10 billion worth of USDC every day.

Goldfinch and stablecoins are pioneering ways to accelerate the speed of commerce and increase the amount and velocity of currency. I suspect that some version of Goldfinch, Circle and other applications will pave the way for DeFi to create real economic value. Useful DeFi technology is emerging. So far the use cases have mostly been financial engineering. I believe that will evolve.