Crypto Carnage...Where From Here?

Crypto Carnage...Where From Here?

What has changed, needs to change and has not changed...and where we go from here.

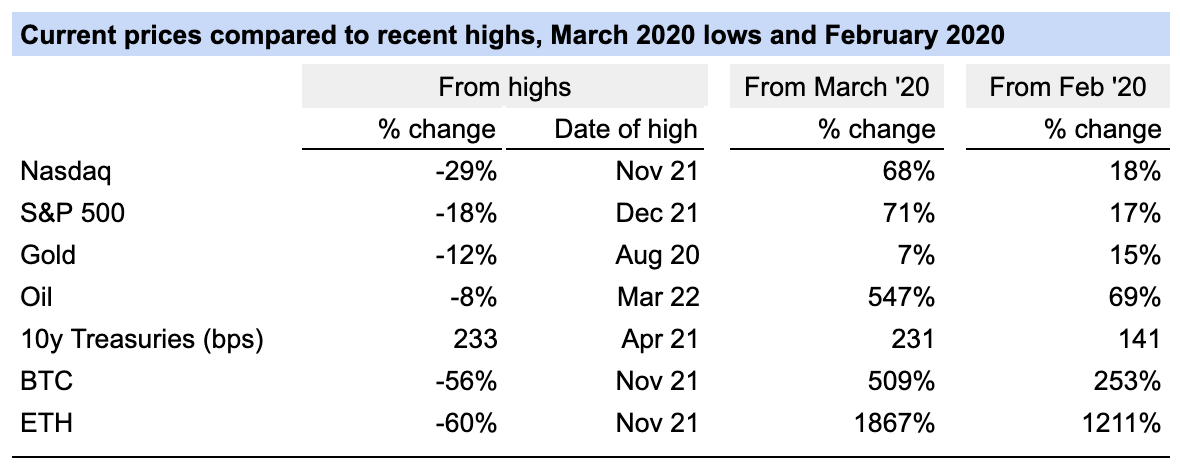

Global markets and crypto are on shaky ground. So far this year $7 trillion has been wiped from the S&P 500 and $1 trillion from crypto markets. From Q4 2021 highs, equity indices are down 20-30% and crypto is down 60%.

A dramatic shift in investor sentiment is taking hold. To fight a 40-year high inflation rate of 8%, policy is shifting from a 40 years of declining rates and a 14 years of multi-trillion stimulus, initiated by the Global Financial Crisis and turbocharged by the response to the Covid-19 pandemic, to a policy of rising rates and no stimulus. There is no longer unlimited money to inflate asset prices.

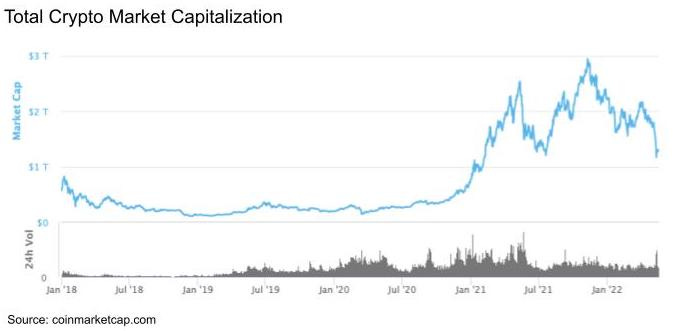

The macro backdrop impacts crypto markets. Terra’s collapse further exacerbated the carnage. To understand what happened with Terra, read WTF LFG...crypto crash explained. In a week, $500 billion of crypto market cap was wiped and $1.7 trillion wiped from November 2021 highs.

I will assess:

The carnage

What has changed

What needs to change

What has not changed

Where from here

Note: I use the term crypto to refer to the broader crypto currency market and web3 to refer to the ecosystem being built on blockchain technology.

The carnage

To assess the wreckage, I’ll put the Terra collapse in context and highlight the fallout from “blue chip” coins, DeFi and NFTs.

Terra

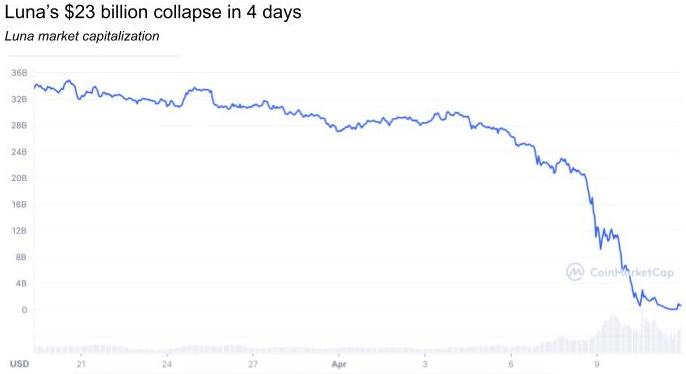

Monday, May 9, 2022 was a historic day in crypto. The third largest stablecoin, US Terra lost its peg and in the subsequent 4 days eviscerated $40 billion of market capitalization from the de-pegging of US Terra and the collapse of Luna.

Lehman Brothers had a market capitalization of $60 billion at its peak in 2007 before filing for bankruptcy in the wake of the Global Financial Crisis. In the fall of 2008, fearing it would go bankrupt and collapse the financial system, the US government bailed out AIG; $180 billion of AIG market cap was wiped out. The combined market capitalization loss of Lehman and AIG represents 1.2% of the pre-crisis total US market capitalization. The total US stock market capitalization declined over 40% from nearly $20 trillion to $11.5 trillion during the Global Financial Crisis.

Mt. Gox was the largest crypto exchange and accounted for 70% of bitcoin transactions until it was hacked. In February 2014, it filed for bankruptcy disclosing that an estimated 744,408 bitcoin, 7% of total outstanding, was stolen. The stolen bitcoin was worth $350 million at the time, which was 3.5% of the total market capitalization of bitcoin. The market capitalization of bitcoin fell from $10 billion in January 2014 to $5 billion by April 2014.

In 2016, when the Ethereum blockchain was a year old, its most notable project, The DAO, was hacked. $60m worth of eth was stolen, which represented 4% of the $1.5 billion eth market capitalization at the time. It was an existential threat. The thief controlled 14% of eth circulation, which undermined the integrity of the blockchain. The eth market capitalization fell by 50%. In a controversial vote, the Ethereum community voted to hard fork the blockchain. It changed its history such that the hack never happened.

The $40 billion Terra collapse is enormous both in dollar size and relative market size. The loss represents 2.7% of the total crypto market cap prior to May 9. As a percentage of market capitalization, it’s bigger than the combined Lehman Brothers and AIG collapse and smaller than the Mt. Gox and DOA hacks. It’s a B.F.D. But it is not an existential risk. It’s an isolated incident that does not undermine blockchain technology. Terra was a house of cards built on uncollateralized faith, unsustainable growth, a radical founder and a desire from market participants for it to work. It’s a painful collapse, yet crypto markets have endured worse.

“Blue Chip” coins

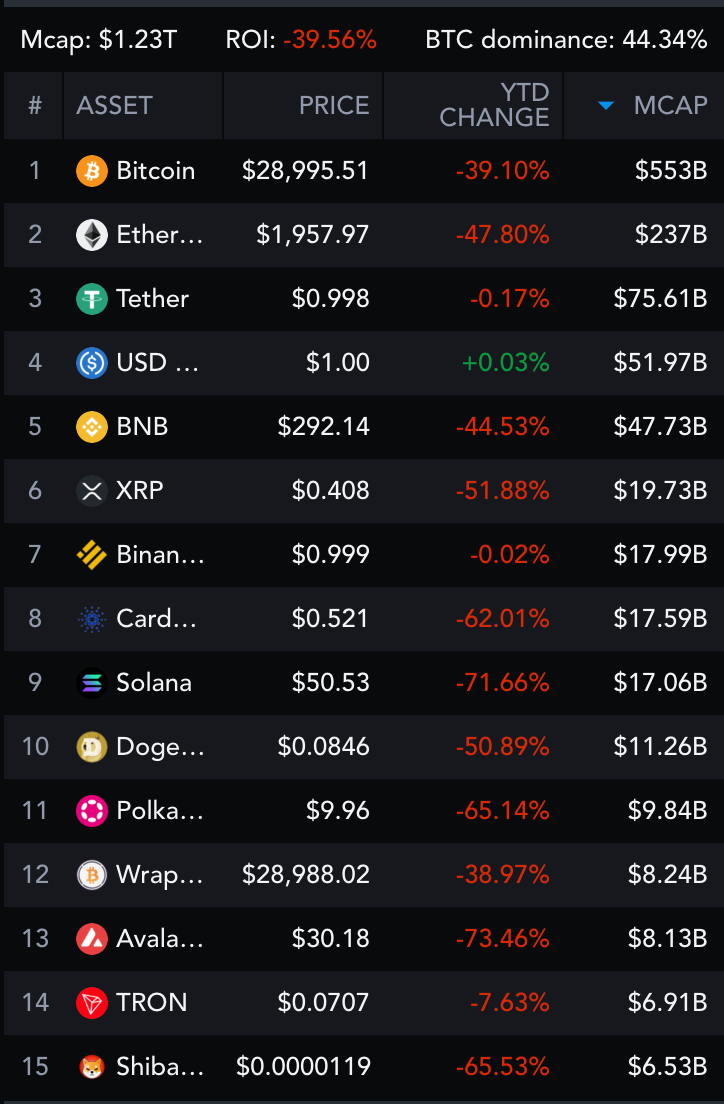

Crypto prices have been selling off since their peak in November 2021. Larger “blue-chip” coins are down 40% year to date.

DeFi

Total Value Locked (TVL), a gauge for the size of the DeFi market, has declined $85 billion from $170 to $85 billion. Of the $85 billion decline, an estimated $68 billion was due to the 40% price drop and $17 billion from assets being removed from the DeFi ecosystem.

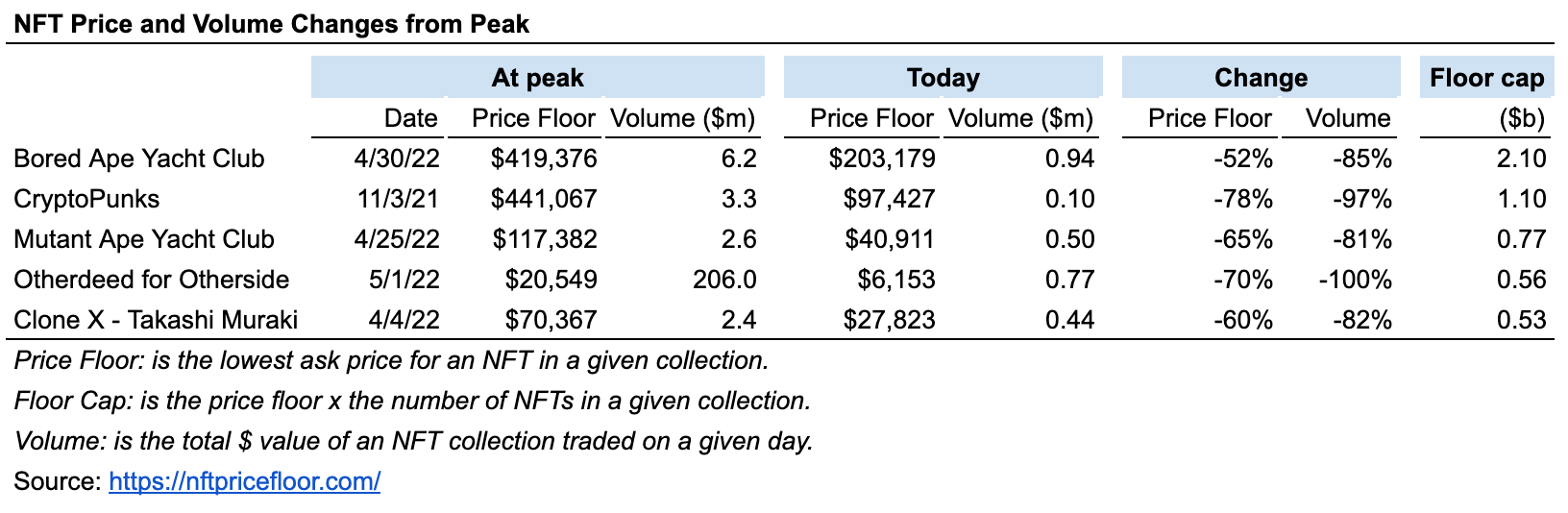

NFTs

The NFT market capitalization (calculated as the sum of the last price of each NFT from all the collections listed on NFTGo) is an estimated $20 billion. Prices for top projects have declined 65% in USD terms and volumes have declined 90% from their highs. NFT sales volumes have declined to under $350m per 4 days from ~$700m last month and a high of $3b at the beginning of the year.

We are in a bear market in all assets. In times of acute market stress all correlations go to 1; everything moves down together at the same time.

What has changed

1. Distrust of ecosystem

The Terra collapse elevated the public’s distrust of crypto to a new level. The fraught economics of UST and Luna have been exposed to the public. $40 billion was lost nearly overnight. Retail investors were acutely hit, some lost their life’s savings. Notable funds including Jump Crypto, Polychain, Arca, Binance and Coinbase Ventures were also hit.

Trust will slowly be built back. The collapse of Terra is an indictment of a specific high-risk sham project. It is not an indictment of blockchain technology. Crypto recovered from Mt. Gox and the DAO hack. Financial markets recovered from the Lehman bankruptcy and AIG bailout. Frauds at Enron, WorldCom and Theranos didn’t end innovation. Ponzi schemes like Maddoff’s didn’t end investment firms.

2. Capital allocation

Large capital allocators will rethink their allocation to crypto because other asset classes have sold off and Terra’s collapse has given crypto a black eye. Google, arguably one the best businesses in the world, grows revenue at 20% per year and trades at 15x earnings. Google has historically traded at mid-20x earning multiple and the market overall usually trades at a high teens earning multiple. There will be less appetite from investors to take on more risk, and venture into crypto, because prized assets are now trading at attractive valuations and can generate good returns.

3. Death of algorithmic stablecoins

Terra’s collapse has spelled the death of algorithmic stablecoins.

4. Regulation is coming

Crypto markets could now be more tightly regulated than previously expected.

5. Investors washed out

Crypto investors lost $500 billion, -30%, in a week. Retail investors will not rush back in after getting burned.

6. Bitcoin as a store of value

The recent selloff has made it clear that bitcoin is not a store of value for people in the developed world. Bitcoin’s benefits, its transferability and immutability, are not that valuable for those in the developed world. Especially when the cost of those benefits is a 40% decline in value year to date. Bitcoin is not a competitive store of value asset compared to cash, gold and treasuries. Most people in the developed world are not worried that the government is going to seize their assets. If they fear inflation they can buy equities and commodities.

However, for those in despotic regimes who fear hyperinflation and the government seizing assets, bitcoin is a good store of value. They are willing to withstand the volatility because the alternative is dyer.

Globally there is $418 trillion of wealth defined as the value of financial assets plus real assets, owned by households minus their debts. I estimate that there is $60 trillion of wealth in regions of the world with despotic regimes. For that wealth, bitcoin is a useful store of value; that’s a gigantic use case for bitcoin.

What needs to change

1. Leverage parameters

Leverage is exacerbating volatility in crypto markets. Although leverage is used in TradFi, there are metrics to gauge how much leverage exists in the system. Budget deficits and debt/GDP are tracked for sovereigns. Corporate debt levels and interest coverage is monitored for companies. Household and credit card debt tracked for consumers. Retail investors are usually capped at 1.5x leverage on their equity portfolio. Most mutual funds and ETFs do not use leverage. Hedge funds, which use leverage, are monitored by their prime brokers providing it to them. It’s not a fool proof system, excessive leverage caused the 2008 Global Financial Crisis and Archegos Capital Management $20 billion implosion in March 2021. But at least there are some metrics to track the use of leverage in the system.

There are no metrics to measure leverage in crypto markets. Professional traders are getting up to 100x leverage. Retail investors can easily get 5-10x leverage from centralized exchanges and get additional leverage from decentralized lending platforms. It’s leverage on top of leverage.

Developing leverage parameters to determine how much crypto is owned on leverage would help assess the financial risk in crypto markets. Reducing leverage would make crypto markets less volatile. Unfortunately, the DeFi innovation has mostly been used by traders to make levered bets instead of loans issued to the unbanked.

2. Valuation heuristics

TradFi analysts can determine the intrinsic value of an asset. When the market price deviates from the intrinsic value great investment opportunities arise. It’s the basis of value investing pioneered by Benjamin Graham and David Dodd and popularized by Warren Buffett.

Crypto participants claim a coin is “cheap” relative to its previous highs. But price is not an indication of value. It is a reflection of the market’s current beliefs. Those beliefs change because information is not equally distributed and markets are irrational.

Crypto needs to develop valuation heuristics to determine the intrinsic value of assets. It would be far easier to step into positions now, if I could determine what these assets are worth. This is one of the most compelling avenues of crypto research.

Without valuation heuristics, crypto investing is dependent on the greater fool theory. Investors, or speculators, buy assets on the basis that a greater fool will buy it from them later at a higher price. It works in bull markets, until there is no fool left to buy; then prices collapse.

3. Tribalism

Crypto needs to drop the tribalism. There are Bitcoin maximalist, Ethereum maximalist, Lunatics (that’s actually the name chosen by those supporting Luna) and maximalists for nearly every blockchain. They are all ardent supporters of their blockchain and tear down others. Twitter is awash with maximalist hurling insults at one another.

The tribalism is an affront to the decentralized inclusive community web3 aspires to be. It detracts from mainstream adoption. It needs to go.

What hasn’t changed

1. Underlying Technology

Programmable blockchain technology has not changed. Blockchains are valuable because of four key features:

Decentralized: No one entity controls a blockchain creating “trust-guarantees” that foster cooperative networks. It also allows for self-custodied assets, which create a better user experience.

Functional: Blockchains are programmable, immutable, transparent and permissionless, which provides more latitude for developers to build applications on.

Composable: Blockchains are composable meaning each component can be recombined into another, which facilitates and accelerates innovation.

Native economics: Blockchain native tokens allow for value to be created, stored and transferred natively online.

Combined, these features spur The Innovation Supercycle.

2. Investing landscape

The reason crypto is a fertile investing ground is:

Inefficient market: Crypto markets are opaque. There is no standard reporting and historical data is limited. Opaque markets are inefficient and ripe with opportunity (and scams).

Research edge: By doing your own research you can develop an edge because i) few others are doing the work, ii) unlike traditional markets there are no set heuristics, you need to develop your own novel thinking.

Less competitive: Hedge funds spend billions on data and AI to develop an informational edge. That doesn’t exist yet in crypto. The largest pool of great investors are at private equity, venture and hedge funds because that’s where the money and job security is. Alternative asset managers, mostly private equity, venture and hedge funds, manage $9 trillion. There are fewer sophisticated investors in crypto because it’s an emerging market that requires learning something entirely new - and that’s hard, especially for those schooled in traditional finance.

Access to previously private deals: Native blockchain tokens allow investors to invest and participate in projects at an earlier stage. Previously that was reserved for Limited Partners of funds.

Tailwinds: Blockchain has the potential to disrupt existing industries and develop new ones. Picking a sector with the tailwinds is key to investing. Growth tailwinds will offset inevitable mistakes.

Where from here?

The influx of talent and capital and crypto adoption will drive where things go from here. Let’s break down each one.

1. Talent

“What the smartest people do on the weekend is what everyone else will do during the week in ten years.” Chris Dixon, Partner a16z.

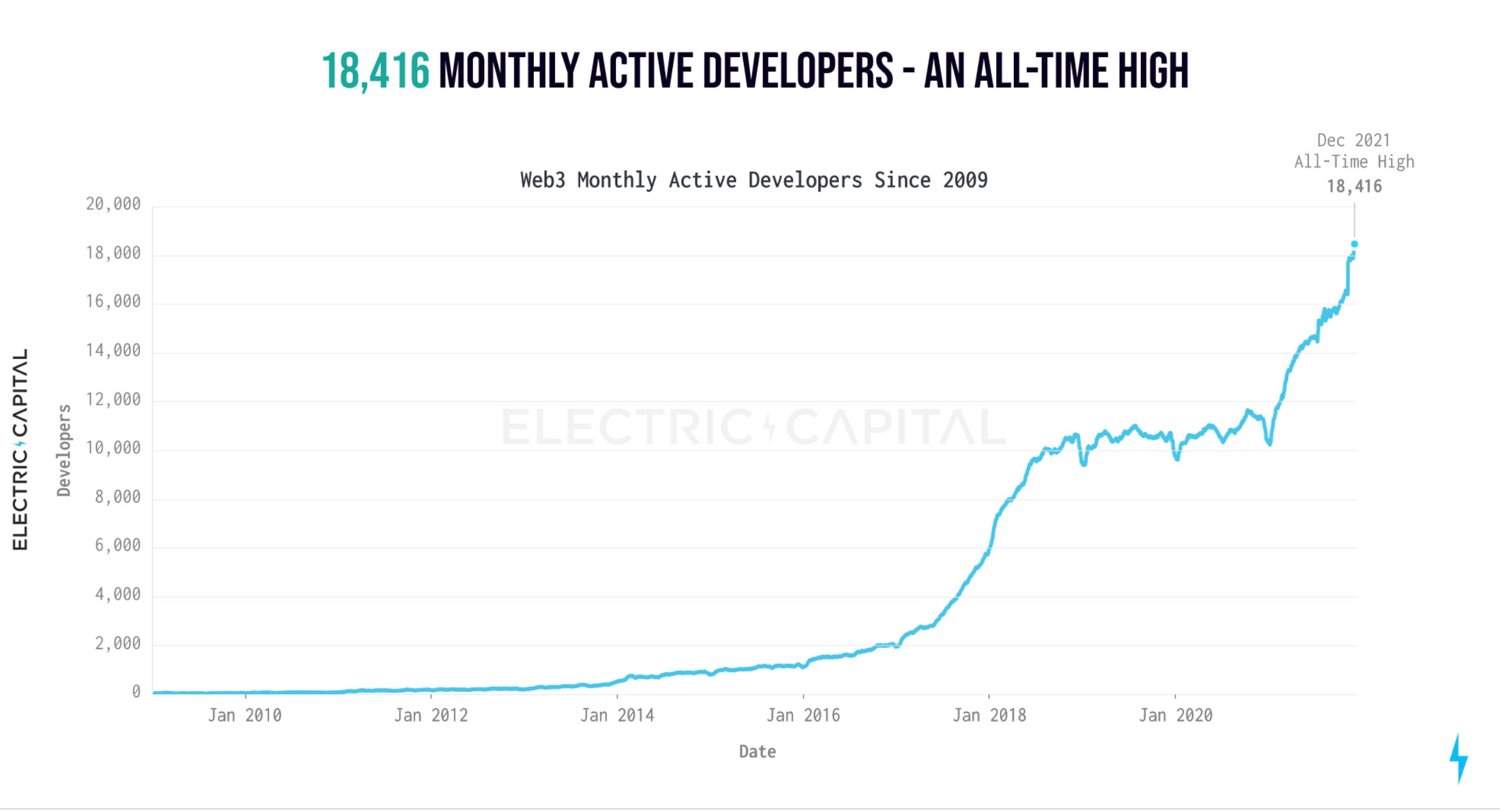

There is an influx of talent into crypto/web3. It’s moved out of garage hobbies to a $1.3 trillion industry. Following developers, and particularly their growth, is a leading indicator of potential adoption and product innovation.

The number of monthly active developers in web3 hit a high of over 18,000 in December and grew 75% in 2021.

Encouragingly, the number of monthly active developers remained constant during the bear market of mid 2018 to mid 2020, which bodes well for the most recent drawback.

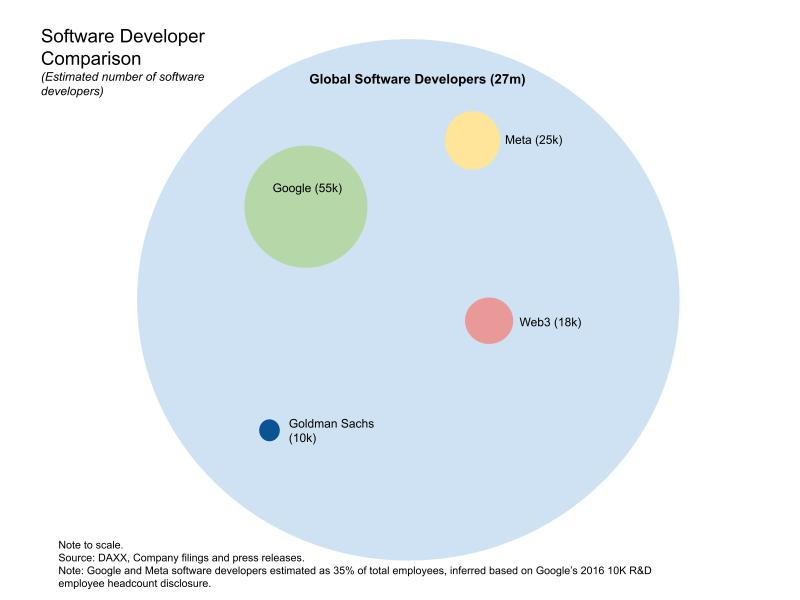

There are nearly 27 million software developers globally. The largest tech companies each employ an estimated 25,000 to 55,000 software developers. Although the 18,000 developers in web3 is minuscule in comparison, it’s growing at a +70% CAGR (admittedly in bursts when prices are soaring). The small number of web3 developers have an outsized impact. They created a $1.3 trillion market, which is $71 million in market capitalization per developer and 2.6x the market capitalization/developer of Google.

Github is the best source for estimating the number of developers in the ecosystem. Active monthly developers, defined as original code authors on github that make monthly commits of new open source code, are the closest thing to full time employees. In addition, there are over 34,000 new developers that committed code in 2021, which is 1.5x up from 2020 and 14% higher than the prior peak in 2018. Those are people that contributed one-off code; think of them as part time or project based workers.

2. Capital

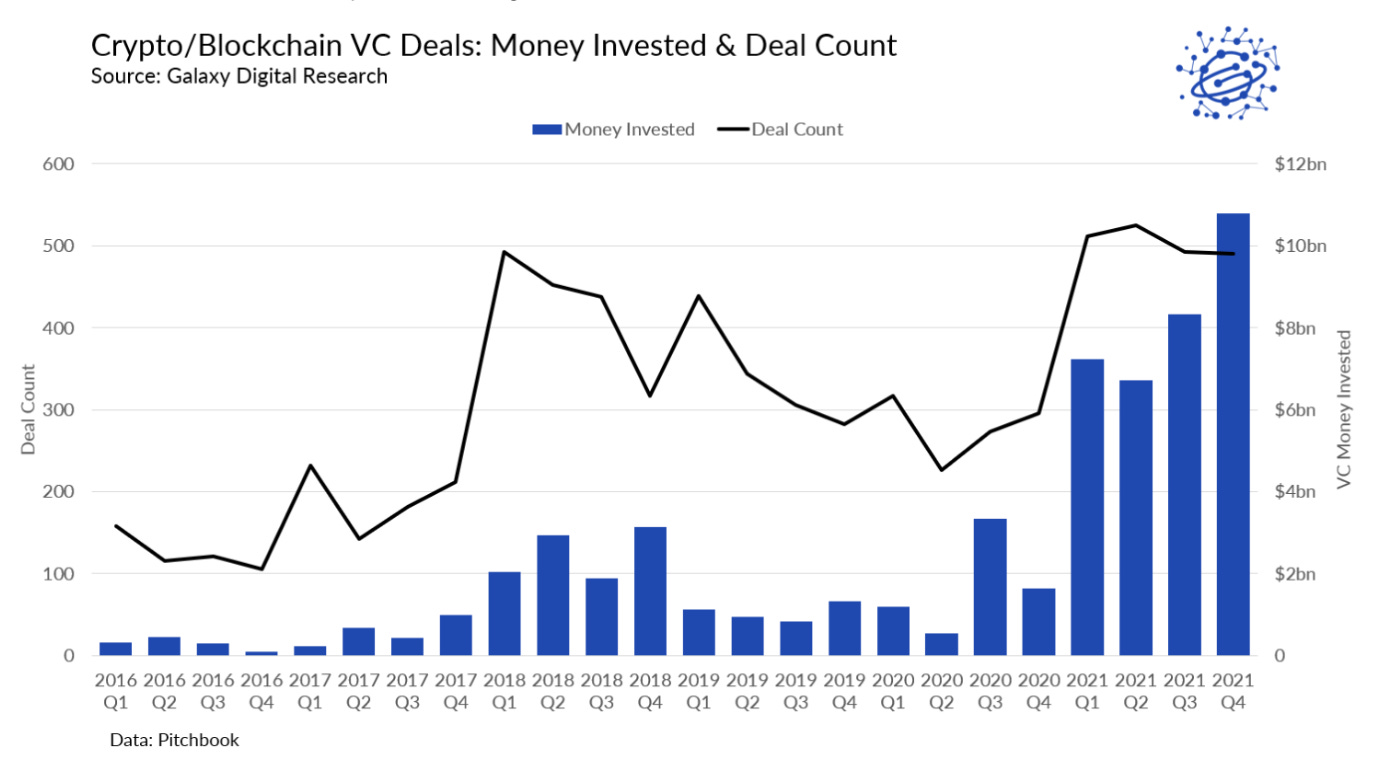

A growing capital pool to invest in a crypto/web3 projects is an emerging endorsement of the space. Capital deployed and raised and institutional interest are signs of a changing interest in the space.

Venture capitalists deployed $33 billion in crypto startups in 2021, which is more than in all prior years combined. Crypto startups received 5% of all venture capital deployed. The growth continued in Q1 2022 setting a new record with nearly $15 billion of capital deployed in 514 deals.

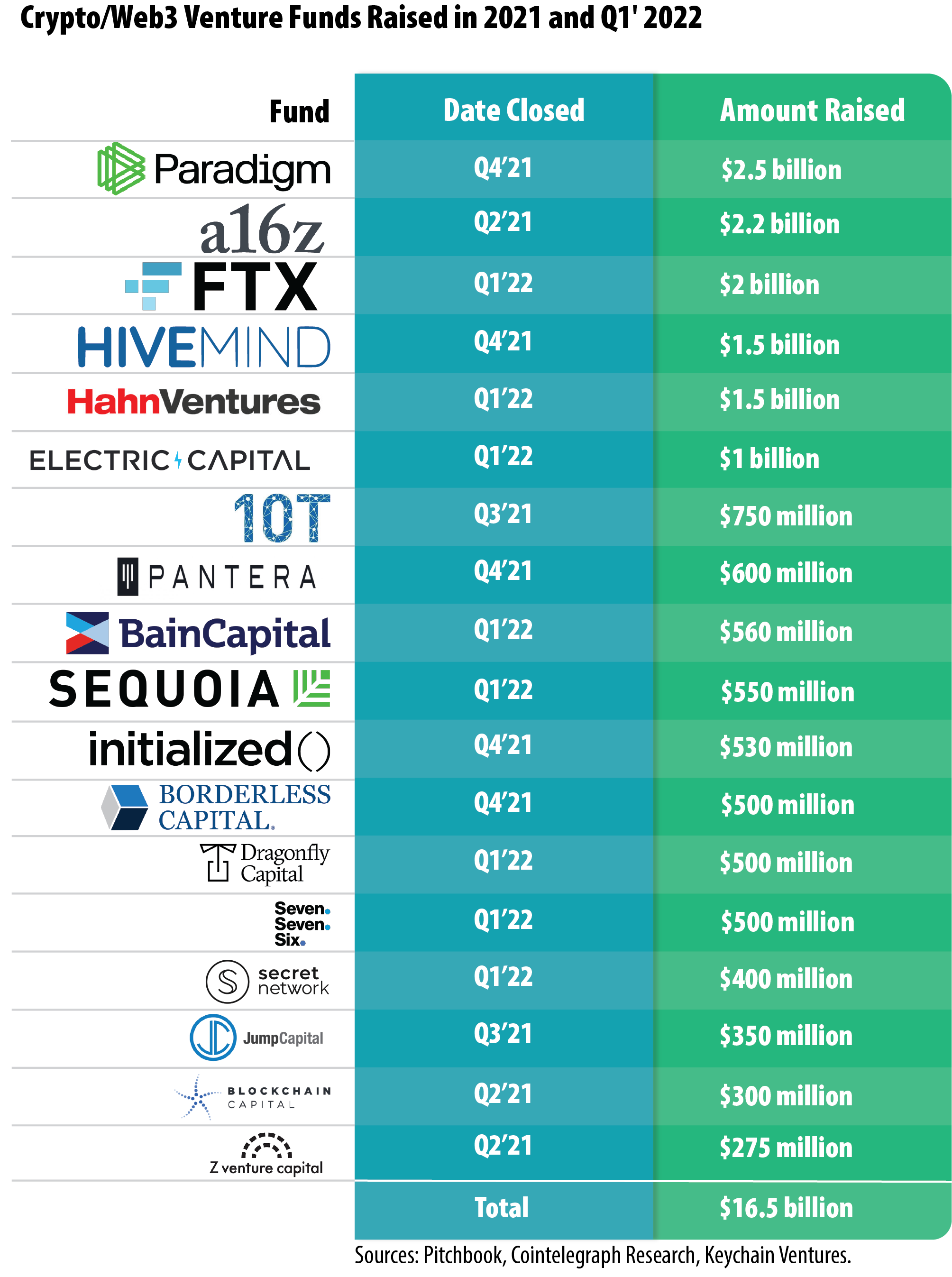

Several notable funds have raised a total of $16.5 billion in 2021 and Q1’2022 to invest in crypto/web3 startups.

Seeing the inflow of people and capital and hearing demands from clients, traditional financial institutions are getting into crypto. Their interest is a lagging indicator of adoption and marks a potential change in sentiment.

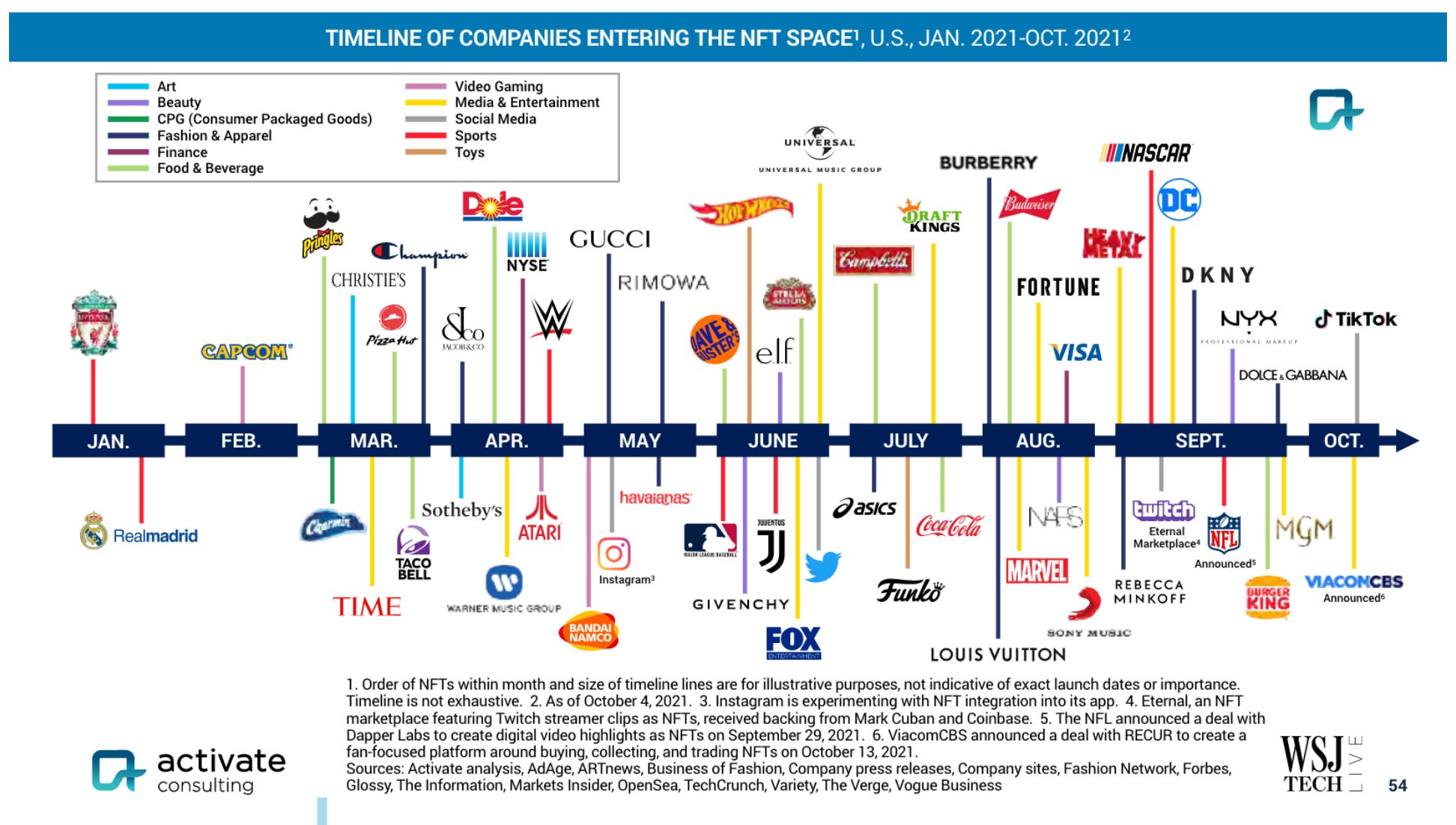

Established consumer companies are actively pursuing NFT projects.

2. Adoption

There are an estimated 295 million crypto owners globally. These figures are approximations derived from extrapolating the number of addresses at 21 exchanges to the entire market. The number of crypto owners nearly tripled in 2021.

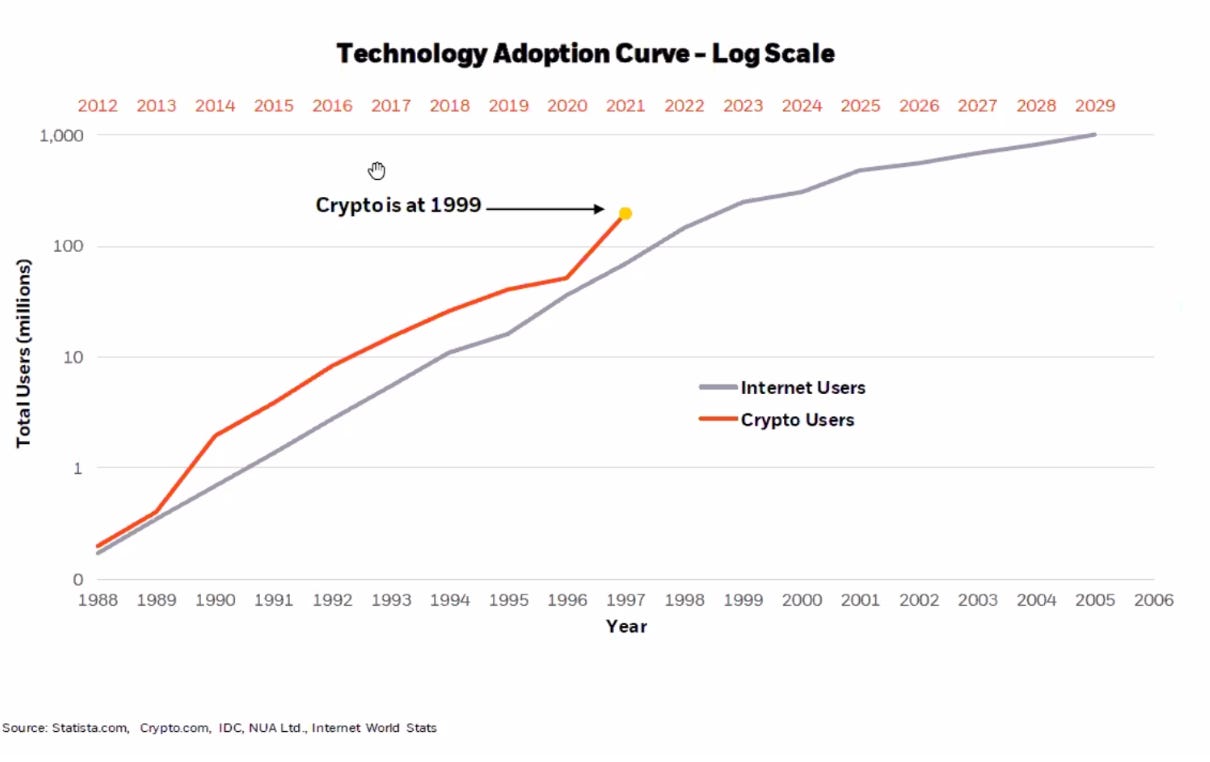

Crypto is growing at a faster rate than the internet was in its infancy. That’s obviously good, but it’s expected. Technological adoption rates accelerate over time. It took over 25 years from the 90s for the internet to be adopted by over 90% of the US population. It took smartphones only 8 years from 2008 to be adopted by 80% of the US population.

The comparison to the number of internet users is a propos, not because web3 will replace the internet, but because a large number of internet users could interact on blockchains. The internet facilitated communication. Blockchains expand on that by facilitating the creation, storage and transfer of value natively online, which is a form of communication. Of the 5 billion internet users today a lot will use blockchains in the future; a lot more than the 295 million people that use it today.

Tying it all together

There has been a large selloff in global markets due to a paradigm shift in a 40 year rate policy and a 14 year stimulus policy. Crypto markets were battered by the global selloff and acutely impacted from Terra’s collapse. Terra is a big deal, but it is not an existential risk. Crypto markets have withstood worse. Some things will change for the worse: distrust, capital allocation, investor chagrin and bitcoin as a store of value. Some possibly for the better: regulation. In time, prices, sentiment and trust will recover because some things haven’t changed: the technology and the investment opportunity. Hopefully as the market matures some things will change: leverage metrics, valuation heuristics and tribalism.

Crypto will go through a 6-24 month downturn. DeFi in particular will be in purgatory. Three factors will help crypto ride out this downturn:

Influx of talent that has shown a willingness to stick it out through prior cycles.

Well funded projects and additional VC capital to deploy.

Interest, albeit tepid, from global companies in TradFi and NFTs.